by Sheila Cox, Five Star Realtor ¦ Updated April 2026

This fantastic First-Time Home Buyer’s Guide, by Sheila Cox, is a 50+ page guide with multiple checklists and lots of tips and advice about buying a home, including:

The benefits of home ownership

Are you ready for home ownership?

Planning Your Timing

Understanding Down Payments and PMI

Do you know what it costs to buy a home?

How to budget and plan to buy a house

Need help with the down payment cash?

Analyze your net worth

How much can you afford to borrow?

How to find a reputable lender

How to improve your credit score

Texas Home Buying Process

Planning the Move

Real Estate Glossary

When You Are Ready to Tour Homes

When you are ready to tour some homes, then call/text me so we can get you on the calendar and discuss exactly what will be the perfect home for you. As a Katy real estate agent (an expert!) I can narrow your focus and help you find the perfect neighborhood.

Once I set up your custom search, then you will start getting home listings via email and you can mark them with Hearts to mark your favorites. A couple of days before our scheduled tour, I make appointments for your Favorite homes and print out the maps, home data, etc. for our tour. On the day of our tour we will meet at my office and then drive the area together so I can tell you about the area and point out various features while also touring homes. This is a great way to find your perfect home!

Newcomers this to area always ask me, "What is a MUD?" In most parts of Fort Bend County, neighborhood infrastructure is provided through a Municipal Utility District, commonly called a MUD. A MUD is a special-purpose local government entity created under Texas law to finance, build, and maintain essential utilities ... [Read More]

Home readiness survey YES NO Do you have enough cash to make the down payment and cover the other costs of buying a home? Does your monthly budget have room to afford the mortgage payment? Do you have a burning desire to own your own home? Is your job/business/income ... [Read More]

Do You Know What It Costs To Buy a Home in Texas? It’s one thing to want to own your own home…it’s another to be able to afford one. Here is a run-down of estimated costs to buy a home in Texas you must consider... Understanding Down Payments and ... [Read More]

If you are buying a home in Texas, then you need to learn about the home buying process, which may be different than other states. One thing to consider is that before you even begin the process of searching for a home, you must: Determine how much house you can ... [Read More]

by Sheila Cox, Five Star Realtor | Updated April 2026 One thing I've found as a real estate agent: most people need help with their home buying timeline. So my recommendations are listed below. Home Buying Timeline for a Resale Home Start with a Deadline. That’s the date you absolutely ... [Read More]

Buying a home is a serious legal commitment with important deadlines and possibly large financial losses if you do not meet your contractual deadlines (as established in the contracts that you sign). Always make sure you read the docs you are signing. Discuss deadlines with your real estate agent ... [Read More]

"That's what I used to think! In fact, before I became a licensed real estate agent, I did several FSBO (For Sale By Owner) sales and THOUGHT I knew what I was doing. But if I had known then what I know now...I never would have risked it. Here's what ... [Read More]

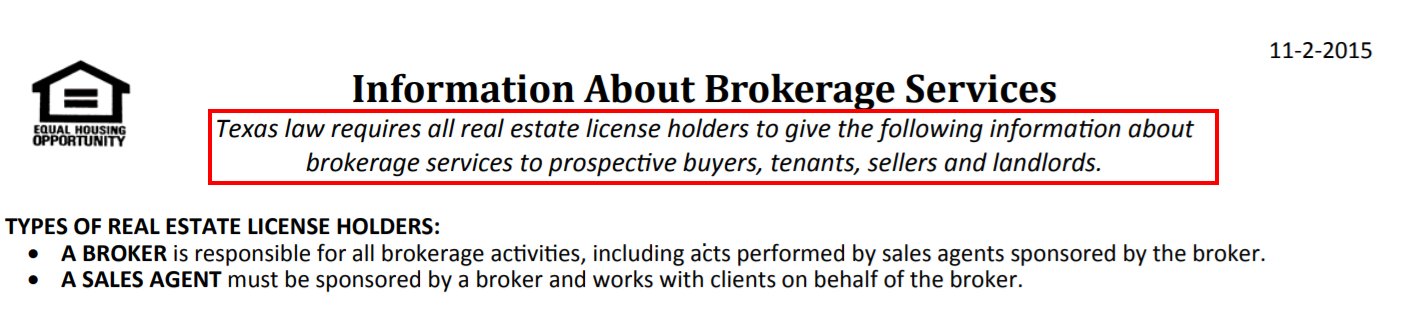

What To Look for In a Katy Real Estate Agent Want to know how to hire the best Katy real estate agent? See below! NOTE: Many of these items are specific to Texas agents. ___ Did your agent give you the "Information About Brokerage Services" notice that is legally required by the ... [Read More]

Does My Real Estate Agent Represent Me or the Seller? When I bought my first house in the mid 1990s, Texas was kind of a "Buyer Beware" state. In fact, a home Buyer could spend weeks looking for a home with a real estate agent, telling her secret information (like ... [Read More]

This information about buyer representation in Texas is so important that the Texas Real Estate Commission REQUIRES that we discuss this before seeing houses. Click image above to see entire document Things Are Different in 2024! There are BIG changes hitting the entire real estate industry as of August 2024, ... [Read More]

Who Pays the Real Estate Commission in Texas? One of the questions that I'm frequently asked is, "Who pays the real estate commission in Texas for a real estate transaction?" That's a good question! Here's the answer... Things Are Different in 2024! There are BIG changes hitting the entire real ... [Read More]

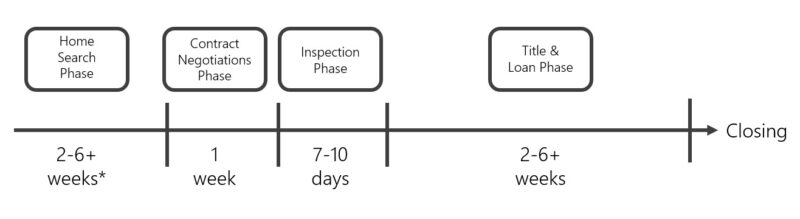

You need a PreApproval letter to start the home search phase in the home buying process in this area because: You need to know exactly how much house you can afford and a lender is the best source for that information. You won't be able to make an offer on ... [Read More]

About the "Due Diligence" Option Period in Texas In Texas, you can buy an "option period" (usually 7 to 10 days) from the seller for $300-$1000 that gives you the irrevocable privilege to back out of the sales contract for any reason, and still receive your 1 percent earnest money ... [Read More]

In a hot real estate market, where homes are getting multiple offers within a few days of being listed, you need to know how to make your offer to purchase a home more competitive. The more you want the home, the more competitive you will want to make the offer ... [Read More]

by Sheila Cox, Five Star Realtor | Updated April 2026 Pricing a Katy home correctly is more complicated than simply comparing the list price to the sales price. Clients often ask me how much they should pay for a home, and I tell them, “It depends on how much it’s ... [Read More]

Here are some helpful tips for Buyers when negotiating a sales offer on a home: Find out the number of days the house has been “on the market” (also referred to as DOM: Days on Market) as well as the pricing history of the home. In Texas, only members of ... [Read More]

The Problem Regarding Real Estate Appraisals One troublesome aspect of home buying and selling is how to handle low real estate appraisals. A real estate appraisal is an estimate of the market value of a piece of real estate based upon a variety of factors. In the definition above, notice the word ESTIMATE. If ... [Read More]

Please know that a home inspection is one of the most important parts of buying a home. But it can be overwhelming trying to find a reputable inspector who you can trust. I provide all my buyer clients with a list of licensed home inspectors in the area to make ... [Read More]

Before a home owner puts a brick home on the market to sell in the Katy TX area, a thorough inspection on the exterior of the home should be performed. All the walls should be checked for cracks along mortar lines and brick. The lintels above windows and doors should ... [Read More]

Will Prior Foundation Repairs Effect a Home's Resale Value? In Texas, there is a saying that all houses here either have foundation repairs or will need them in the future. That's because the soil in most parts of Texas is an "expansive soil" that significantly expands and contracts based on ... [Read More]

When you purchase a resale home, you can purchase a home warranty (a.k.a., Residential Service Contract or RSV) that will protect you against most ordinary flaws and breakdowns for at least the first year of occupancy. The warranty may be paid for by the Seller for the first year. That ... [Read More]

—by Sheila Cox, Five Star Realtor | Updated April 2026— Katy TX Property Taxes--Unfortunately, property taxes in Texas are among the highest in the country. But before you panic, just remember that we don't have a state income tax in Texas...so one sort of offsets the other. I tell my ... [Read More]

A real estate “Closing” is where you and I meet with some or all of the following individuals: the Seller, the Seller’s agent, a representative from the lending institution and a representative from the title company, in order to transfer the property title to you. The purchase agreement or contract you ... [Read More]

As a homeowner in Texas, your Homestead Tax Exemption is a large exemption to reduce the amount of property taxes you pay. Applying for a Homestead Tax Exemption (more info) is a one-time activity in Texas that homeowners need to do the first year they buy a home…not something you do every year. The deadline is not until the ... [Read More]

Katy Home Security: Tips for Securing Your Home That Are Not Well Known If you are interested in Katy home security, then let me tell you my story... A while back I had the unfortunate experience of having my home burglarized. I thought my home was pretty safe: It’s in ... [Read More]

It’s the American dream…to own your own home. But have you considered the specific benefits of home ownership? Studies show the following benefits for home owners: Improved tax advantages…thereby lowering your overall tax burden. Forced savings program (in the amount of principal paid each month on the mortgage)…especially if the ... [Read More]

Are you unsure about becoming a HOMEOWNER? Thinking that you can't afford to BUY a home? Are you worried about whether home buying is a good INVESTMENT? Buying a first home can be an intimidating process. But the first step is making those first decisions: I want to own ... [Read More]

—by Sheila Cox, Five Star Realtor | Updated April 2026— One question that I get a lot is, "What's recommended: buying new vs resale home in Katy?" A new home is one that has never been lived in while an existing home has been lived in by a previous owner ... [Read More]

So you have put a contract to buy a new construction home with a builder and you can't wait to move in. Buying a home is exciting, especially if you are a first-time home buyer, but buying a brand new home that has never been lived in doesn't mean the ... [Read More]

The bottom line: No one knows an area better than a local, experienced real estate agent. Don't gamble your biggest investment on automated Internet data. It's Not All About the ZIP Code...Or Shouldn't Be I love the Internet and I'm an information junkie, but I am constantly amazed at how ... [Read More]

by Sheila Cox, Five Star Realtor | Updated April 2026

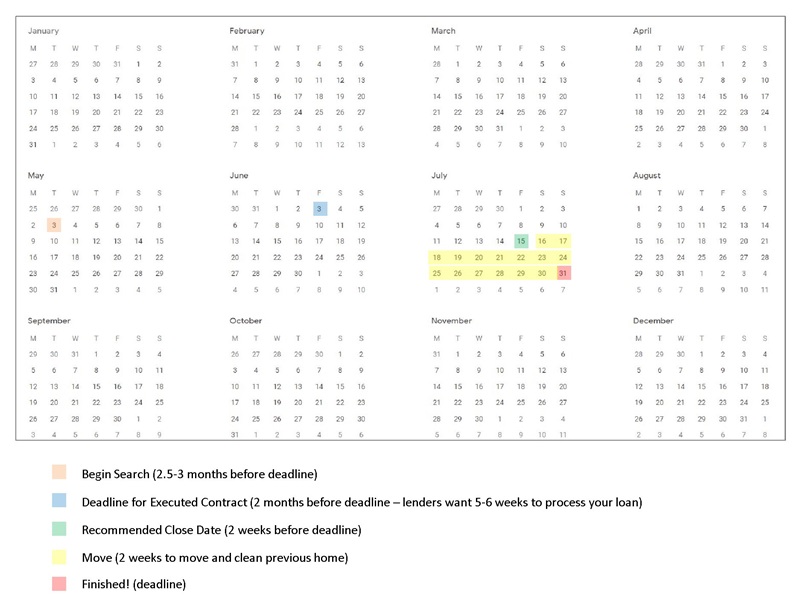

One thing I’ve found as a real estate agent: most people need help with their home buying timeline. So my recommendations are listed below.

Home Buying Timeline for a Resale Home

Start with a Deadline. That’s the date you absolutely have to be out of your current home/apartment. This Deadline may be the end of a lease or a move-out date for an existing home that you are selling.

Begin Search. You should begin your search approximately 2.5 to 3 months before your deadline. Keep in mind that most home owners will want you to Close within 5-6 weeks of executing a contract because that’s the typical time it takes for a lender to process your loan. It may take several weeks before you find a home and get an accepted contract. Some people start their search even earlier, to have more cushion, but they must be prepared to Close early and pay two house payments until the end of their current lease or move out date on current home. (Actually, you don’t usually begin paying a new mortgage for at least one month after Closing. So if you Close in the middle of June, your first house payment may not be until August 1.)

Deadline for Executed Contract. You must be “under contract” on your new home at least 6 weeks before your deadline but 8 weeks is preferred. Again…this is to allow time for your lender to process the loan (usually 5-6 weeks). You should allow a 2 week gap between Closing on your new home and moving out of your current home in order to give yourself time to pack, move, and clean. NEVER plan to Close and move out on the same day. Closings don’t always happen on time, as scheduled. There can be delays caused by the lender. You do not want your belongings on a moving van before you have a definite place to put them!

Recommended Close Date. You should Close on your new home about 2 weeks before your Deadline to move out of your existing home. However, this will need to be negotiated with the Seller of the new home. If they have already vacated the property, they will want a quick/short Closing date. If they are still living in the home, they may want a longer date before Closing or they may want a Temporary Lease to live in the home, after Closing, to have time to pack and move.

Home Buying Timeline for a New Construction Home

This timeline is for purchasing a resale home. If you are buying new construction (home being built from “dirt”) then it will take 5-6 months or more. Keep in mind that there are sometimes material shortages and supply-chain issues, and some home builders have delays. Rainy weather can also delay a Closing date for new construction homes.

Are you worried about whether home buying is a good INVESTMENT?

Buying a first home can be an intimidating process. But the first step is making those first decisions: I want to own my own home; I can afford to own my own home; owning my own home makes sense for me financially and emotionally. If you are still struggling with those first decisions, here are some facts that might help you make that first step towards becoming a homeowner.

You Can’t Afford NOT to Buy a Home!

Over the last ten years, the cost of rental housing in the U.S. has increased an average of 3 percent per year. That means that an apartment or home renting for $750 per month will cost more than $978 a month in ten years. If you rent the same home for ten years, the total amount you would pay for rent will equal $103,000!

Tax Advantages of Owning a Home Result in Savings

None of that $103,175 is returned to you, either through savings or as an investment. Homeownership, on the other hand, has tax advantages over renting a home, and those advantages can help you save money. Unlike your monthly rent, part of your monthly mortgage payment “comes back to you” in tax savings. Here’s an example:

You purchase a home that costs $110,000 (plus closing costs – expenses incurred to actually process the transaction). You finance the balance with a 30-year fixed rate mortgage at 6.5 percent interest. Your monthly payments (not including utilities, maintenance, insurance, etc.) are:

You actually save $195 a month by owning your own home. On a yearly basis, the savings is even more dramatic:

Homeownership is a Good Investment

For the majority of Americans, their home is their largest financial asset and a major player in their investment portfolio. It’s a good thing, too, since stock market value has declined since 1998, while home price appreciation has increased. The NATIONAL ASSOCIATION OF REALTORS® estimates that home value rises, on average, by 4.5 percent a year. That’s a steady return on investment; one’s own home is a much less volatile asset than stocks, bonds or mutual funds.

As an example, let’s look again at that $110,000 home. Unlike your rental unit, your home should appreciate over time. Assuming a 4.5 percent appreciation rate, your home will be worth $114,950 in the second year of ownership, $120,123 in the third year of your owning it, etc. After ten years, your $110,000 home will be worth $163,470. Not only do you earn a rate of return on your original purchase price, but you also get a return on any subsequent appreciation.

Homeownership Builds Wealth for Households

The Federal Tax Reserve Board estimates that homeowners have a net worth almost 36 times more than that of renters. In 2001, the median net worth for homeowners was $171,700 compared to $4,800 for renters. How do you build up your net worth? Through those “appreciating returns” on your home.

We’ve already seen how your $110,000 home is worth $163,470 in ten years. In addition, you are paying down the principal on your mortgage. Remember that $100,000 you borrowed at 6.5 percent over 30 years – that debt amount is decreasing every month and every year.

After the first year, you now only owe $98,786 on a home that is worth $114,950. You have “netted” a $4,950 increase in the value of your home, plus $1,116 a year that previously you owed as part of your mortgage debt. As your debt decreases and the home value increases, you accumulate wealth from the value of your home. In addition, over this ten-year period, you will have a significantly lower after-tax payment for housing. Each year as your home appreciates and you continue to pay down your mortgage debt, you increase your own net worth.

Homeownership – It’s NOT Just About Money

The “numbers tell the story” should ease your mind about the financial aspects of becoming a homeowner. But there are other, less monetary, benefits to homeownership. Several research studies indicate homeownership adds to the value of communities, has positive effects on children, and even contributes to increased voter participation rates.

—by Sheila Cox, Five Star Realtor | Updated April 2026—

One question that I get a lot is, “What’s recommended: buying new vs resale home in Katy?” A new home is one that has never been lived in while an existing home has been lived in by a previous owner. There are Pros and Cons either way that you should consider. Here are my home buying tips for buying a new vs resale home.

PROs for Purchasing a New Home May Include:

Lower maintenance costs during the first years of owning the home.

Lower energy costs because new homes are built with better energy saving materials and equipment than older homes.

More functional home designs and floorplans as well as up-to-date home fixtures.

Latest technology features such as pre-wired for a home computer network.

Possibly the ability to choose paint colors, floor types and colors, exterior colors, and other optional home features.

NOTE: There is typically a substantial markup on these items.

Builder incentives to lower the initial cost to purchase.

Easier to get to know neighbors because everyone is “new.”

PROs for Purchasing an Existing (Resale) Home May Include:

Lower price per square foot than newly built homes.

Better locations and shorter commute times.

Mature landscaping in both the yard and throughout the neighborhood.

Proven track record of home values in the neighborhood.

Lower tax rates since more neighborhood features have already been paid for by home owners.

Sales contracts that are fair to both parties…not one-sided in favor of the builder.

Lower move-in costs (possibly) since home already has window coverings, landscaping, garage door openers, and other items that you will have to buy for a brand new home.

Easier for home inspector to find home defects because more time has passed since the home was constructed. NOTE: New homes may have hidden defects that are impossible for a home inspector to find.

More established school zone boundaries than for new neighborhoods.

Established community activities and events.

Quicker move-in date compared with building a home from scratch in a new neighborhood.

If you decide to buy a new home, make sure that you check out the builder first: http://houston.bbb.org/consumers/. Also make sure that you hire an inspector.

And don’t forget to bring your Realtor along when you view new home models! Remember: A Realtor’s job is not “just” helping you find a house to buy…there are over 100 tasks that Realtors may perform for you during the home purchase process! Your Realtor should be on your side because she is your agent. The salesperson at the builder’s model home office is not on your side and has no Fiduciary Duty to you. As an employee of the builder, he or she is looking out for the builder’s best interests.

Before you decide to buy a new home, make sure you get up-to-speed on new home builder’s warranties at:

I don’t want to discourage you from buying a new home…Houston has some really great new home builders. But it’s my job to make sure that you have all the information that you need to make a wise buying decision.

Buying a home is a serious legal commitment with important deadlines and possibly large financial losses if you do not meet your contractual deadlines (as established in the contracts that you sign). Always make sure you read the docs you are signing. Discuss deadlines with your real estate agent and put them on your calendar.

Checklist for Home Buyers

Print this checklist and use it to keep track of your transaction.

This list is not comprehensive. There are a lot of steps that your REALTOR® takes care of behind-the-scenes.

Action

Deadline

Contact three or four lenders to determine how much house you can afford. Determine how much money you will need to purchase a new home. Do you have enough? If not, create a budget and start saving now.

Get approved for a loan. Don’t forget to get an preapproval letter! We will need to submit it with an offer to buy a house.

Hire a real estate agent to help you with your purchase. You need a professional looking out for your best interest. Send your Preapproval letter or “Proof of Funds” to your agent (see video).

Do you need to sell your current home? Your agent will help with that too. Get it on the market!

View “Dream Home Alerts” (see video) for homes when they “hit” the market.

Tour homes (see video) until you find the one that meets your specific needs.

Sign the legal paperwork and make an offer to buy the house that you chose. Be prepared to write check for Earnest Money (see video). Be prepared for some back-and-forth negotiations.

Deliver the Earnest Money and Option fee to the title company. TIME IS OF THE ESSENCE! If you don’t deliver the Option fee on time, then you have NO Termination Option.

NOTE: Learn about Option Periods in Texas (see video).

Once the title company “receipts” your Earnest Money and Option Fee, then send the executed and receipted contract to your lender and start the approval process with him/her.

After the sales contract is executed, hire home inspectors to inspect the home as needed (learn more). This will cost $300 to $700 or more, depending on the number and type of inspectors you hire. Depending on the home, you should think about the following inspections:

Discuss insurability with insurance company and get a CLUE report from insurance agent.

Verify the following if they are important issues to you:

· Square footage of home

· Schools zoned to home (but those may change with rezoning in future)

· Property taxes

· Crime in area (contact police department)

· HOA covenants and restrictions (usually online at HOA website)

Negotiate repairs to home as needed. Be realistic…small miscellaneous items should be expected because no home is perfect. Negotiate big-ticket repairs (if any) or walk-away.

Now that you have exact address, compare mortgages and lenders (at least three is recommended). Choose a lender and mortgage and apply for a loan if you haven’t already. Remember, you have a deadline to meet in the sales contract. Be prepared to pay an application fee (approximately $300) and an appraisal fee (approximately $300-400).

Submit items for your loan application (W2s, tax returns, pay stubs, bank statements, etc) as requested by your lender. Time is of the essence! According to the contract, your deadline for Individual Approval and Notice to a Seller (from lender) is à

If you do not get loan approval, then notify your real estate agent immediately.

Check your Title Commitment (learn more) in a timely manner when you receive it. You have only a few days to “object in writing.” Make sure your real estate agent receives a copy.

Review the Lender’s appraisal in a timely manner. You have only a few days to “object in writing.” Make sure your real estate agent receives a copy.

Review the survey in a timely manner. You have only a few days to “object in writing.” Make sure your real estate agent receives a copy.

Re-inspect home, if you choose, based on agreed repairs.

Obtain home owner’s hazard insurance. Make sure you get at least three quotes. Notify your real estate agent which policy you choose. Don’t forget Flood Insurance!

Select your residential service contract (“home warranty”) if applicable and notify your real estate agent (learn more). The title company will order and pay for the home warranty.

Plan your move (get detailed list) and order your utilities to be turned on the day you Close. Always allow a week or more overlap to move out of current home and into new home. Do not plan to Close and move on the same day!

Ask your lender for the amount of money you need to Close. Make sure your funds for Closing are available at local bank. Transferring money from investment accounts can take time…work with your lender and bank and prepare in advance.

Your property MUST reach Lender Approval at least 4 days before Closing otherwise you may not be able to obtain a refund of your earnest money due to default on Closing. If there is a delay in getting the loan, notify your real estate agent immediately.

Make sure your Closing is scheduled. You will need photo IDs, checkbook, and a cashier’s check or wiring instructions from your bank.

You must sign your Closing Disclosures (from lender) at least 3 days before your Closing date or you will not be able to Close on time. If you do not sign the CD in a timely manner, this may put you in default and there could be serious financial consequences.

Get your cashier’s check for funds needed to Close the day before Closing.

Do your final walk-through.

Go to the Closing and bring your funds to Close, a checkbook, and a photo ID for each person (husband and wife). Plan on a 2-3 hour process.

Move into your new home and enjoy!

Make sure you receive a copy of your Deed (from the Title company) within a couple of weeks after Closing. Be prepared for mail “scams” offering to file legal docs for a fee.

Apply for your property tax exemptions as applicable in your state.

Contact three or four lenders to determine how much house you can afford. Determine how much money you will need to purchase a new home. Do you have enough? If not, create a budget and start saving now.

Get approved for a loan. Don’t forget to get an preapproval letter! We will need to submit it with an offer to buy a house.

When you sign up as my client, I will provide this checklist and more in my Ultimate Home Buyer’s Guide.

The bottom line: No one knows an area better than a local, experienced real estate agent. Don’t gamble your biggest investment on automated Internet data.

It’s Not All About the ZIP Code…Or Shouldn’t Be

I love the Internet and I’m an information junkie, but I am constantly amazed at how WRONG the real estate info presented on the internet is for my area: Katy TX. Katy is a large city (population 250,000+) located in in Fort Bend County, just west of Houston TX. Like all cities of its size…some parts are very different than other parts…it is not completely homogeneous. Furthermore, it consists of multiple ZIP Codes: 77450, 77494, 77493, and 77449. And, Katy is adjacent to Houston, Fulshear, and Richmond as well. So you can live in the Katy area but technically have a Houston address.

What really “bugs” me about the data available on the Internet is that most websites use ZIP Codes to determine demographics and “city data.” But you can’t do that accurately in Katy since it has multiple ZIP Codes. And to complicate matters, Katy is divided into multiple master planned neighborhoods and each of those may be split into multiple subdivisions. For example, Cinco Ranch consists of over 50 subdivisions. So you can have multiple neighborhoods and subdivisions within the same ZIP Code, but let me assure you that the demographics and average income for homes in Avalon Seven Meadows is drastically different than those in Falcon Landing (two subdivisions in the same ZIP Code).

Here are some examples that “bug” me. I’m using information for the nearby Sugar Land TX area, but you get the idea…

At the time the above data was posted on the Internet, I checked the Multiple Listing Service (MLS) database which reported a median list price at $329,000…not $349,440 (as shown above). And besides that…I assure you that we have many subdivisions in Katy where you can purchase a home for much less than that price! Or much more! So what’s the point of this information? And the “median” for 77478 is probably not accurate for a specific home in a specific subdivision.

From MLS

NOTE: Home prices are a constantly moving target…even within the same subdivision. The averages, medians, and such change monthly…depending on current market activity. You have to evaluate the value of a home at the time you are making a purchase. (Which is one of the main services that a real estate agent should provide.) Home appraisals are professional opinions only and are typically only considered accurate for six months.

Neighborhoods Need to Be Properly Defined

At least NeighborhoodScout is trying to look at the neighborhood level (see below)…but they fail miserably. The sections they have segmented are not actual Sugar Land neighborhoods…some sections contain multiple neighborhoods…so the data can’t be applicable for a specific home or subdivision. For example, if you click the area that is supposed to be for Telfair, you will see it includes part of First Colony and those subdivisions are zoned to different schools than Telfair. (And trust me when I tell you that schools are one of the most important variables in determining home values in our area!)

Inaccurate Data Misleads People

Here’s my least favorite source of data (city-data)…notice they report only 9 registered sex offenders in all of 77479. We wish!

FamilyWatchDog reports and maps 64 (unfortunately)!

I REALLY don’t like most of the info on city-data because it reports information from any unknowledgeable “joe” who wants to put it up there. For example, I searched for “telfair sugar land demographics” on Google and the top entry was a city-data thread. In it, various and misleading demographics were reported…

Not accurate at all!

FBISD also consists of Houston addresses…not at all accurate stats for Sugar Land.

I think the City of Sugar Land has the best info on actual demographics for the city…they are getting it from the census data.

Each Neighborhood and Subdivision is Unique

The hard fact is that you can’t really get accurate census type data at the neighborhood or subdivision level. Relying on the data for an entire ZIP Code in our area may be very misleading when it comes to the neighbors you will eventually live next to. The best alternative is to look at the demographics for the Katy schools to which a home is zoned.

Only an Experienced Local Real Estate Agent Can Narrow and Focus Your Search

So if you are a home buyer in the Katy area, you really need the guided expertise of a local real estate agent you can trust to help you buy a home in the RIGHT neighborhood at the RIGHT price. No online searches available to the general public–including HAR.com, Trulia, Zillow, Homes.com–none of them will allow you to do the complicated and focused searches that a real estate agent can perform. Today (March 1, 2018) there are approximately 1291 active listings in Katy reported on the MLS. Do you want to sort through all of them or do you want to focus on the top 50 that most closely match your requirements?

Most Online Real Estate Pricing Data is Not Entirely Accurate and Should Not Be Relied Upon

Let me add that Texas is one of the few non-disclose states. That means that real estate data is not public information…so the online companies like Zillow and Trulia don’t have access to real data. They use tax appraisal values which are usually lower than actual home values. So don’t rely on them! And since online companies can’t get the real MLS data, they report erroneous information. Here’s an example…

Here’s the data reported on Redfin on October 15, 2013…which says it is for the last 90 days and focused on one of our most popular neighborhoods: Telfair.

I ran the sales history on the MLS for the last 90 days, and got the following data.

The top box is for Active Listings and the bottom box is for Sold properties.

So let’s look at the differences…

Redfin Reported

MLS Reported

Median List Price

$502,946

$507,440

Median $/Sq Ft

$143

List = $143.68 but

Sold = $133.28!

Median Sale/List

96.5%

97%

Avg # Offers

1.0

No way to know!

Avg Down Payment

20%

No way to know!

# Sold Homes

48

54

My first complaint is that two reported variables are almost impossible to determine: Avg # Offers and Avg Down Payment.Agents do not report the number of offers on a home. They only have to report an offer when it is accepted and goes “Option Pending” or “Pending” (and sometimes they don’t even do that.) So that variable is completely unreliable and shouldn’t be reported at all.

The Avg Down Payment bothers me too. Agents are supposed to report that number at Closing (when a house sells), but you would have to look at every single transaction (54 over the past 90 days) to record those numbers. I don’t see how Redfin could automate that for every neighborhood…so I don’t trust that number either.

Notice the Median List Price is off by $4,500 and the # Sold Homes is off by 12.5 percent. Also, they report the Median $/SqFt for List Price only…but notice that the SOLD SalesPrice$/SqFt is $10.40 less! So if a buyer used the number Redfin reported to price a 3000sf home, that could have led to the buyer overpaying by $31,200!

NOTE: It really doesn’t matter what the median list price is for a neighborhood…only the sales price should be used to price a home you want to purchase.

And then that gets me into a price discussion which is too complicated to address here. But let me point out that this the median SalesPrice/SqFt and the house you may want to buy could be an above-average home or a below-average home. Do you want to pay the average price for a below-average home? Do you think a seller will accept an average price for an above-average home? The best way to get an accurate view of the value of a specific home at a certain time is to hire a professional appraiser or to engage a really good real estate agent. Not all real estate agents are good at pricing homes…you need a PRO!

Even Zillow Admits They Are Not That Accurate in the Houston Area

In Texas, you can buy an “option period” (usually 7 to 10 days) from the seller for $300-$1000 that gives you the irrevocable privilege to back out of the sales contract for any reason, and still receive your 1 percent earnest money back. This gives you time to have the home thoroughly inspected and find any defects that you cannot live with. It also allows time to negotiate repairs with the Seller. At the end of the Option Period (and the timing is very strict) you can do one of the following:

If you “exercise” your option, you lose your option fee, but you get your earnest money back.

–Or–

If you do not exercise your option, then the option fee is usually applied toward your closing costs.

Please know that a home inspection is one of the most important parts of buying a home. But it can be overwhelming trying to find a reputable inspector who you can trust. I provide all my buyer clients with a list of licensed home inspectors in the area to make this process easier for you. Plus, I will negotiate necessary repairs for you with the selling agent…before you close on the home.

In addition, we have many great homes in the Katy area, but some of them may need your personal touch. It’s difficult to estimate these costs ahead of time or to know who to hire. I can help by estimating costs and by recommending local contractors who provide good quality service at reasonable prices. Plus, since I have remodeled many homes myself, I can help answer questions that you may have and get you going in the right direction.

Make sure you hire a real estate agent who knows how to properly handle Option Periods and protect your money!

It’s one thing to want to own your own home…it’s another to be able to afford one. Here is a run-down of estimated costs to buy a home in Texas you must consider…

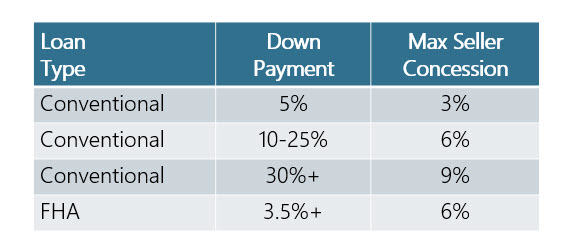

Understanding Down Payments and PMI

PMI – Private Mortgage Insurance

“PMI is a type of mortgage insurance that buyers are typically required to pay for a conventional loan when they make a down payment that is less than 20% of the home’s purchase price. Many lenders offer low down payment programs, allowing you to put down as little as 3%. The cost of that flexibility is PMI, which protects the lender’s investment in case you fail to repay your mortgage, known as default. In other words, PMI insures the lender, not you.

PMI helps lenders recoup more of their money in a default. The reason lenders require the coverage for down payments below 20% of the purchase price is because you own a smaller stake in your home. Mortgagers are lending you more money up front and, therefore, stand to lose more if you default in the initial years of ownership. Loans insured by the Federal Housing Administration, or FHA loans, also require mortgage insurance, but the guidelines are different than those for conventional loans (we’ll cover that later).”

The following example is for a $360,000 home with a 3.5% interest rate conventional 30-year mortgage. Includes $8000 property taxes and $2000 annual home owners insurance (both are estimates…amounts vary depending on home).

It’s one thing to want to own your own home…it’s another to be able to afford one. Here is a run-down of estimated costs you must consider when buying a new home.

Please note these are estimates only and will change based on the area where your home is located, price of home, lender requirements, negotiated terms on sales contract, etc.

The following estimated example is for a $360,000 home with 5% down payment with a 3.5% interest rate conventional 30-year mortgage. Includes $8000 property taxes and $2000 annual home owners insurance (both are estimates…amounts vary depending on home).

Item

Estimated Cost

Your Cost

Purchase Price

$360,000

Down Payment (5%)

$18,000

Loan Amount

$342,000

TO MAKE AN OFFER & INSPECT HOME

**Earnest Money (typically 1% of purchase price)

$3600

**Option Fee (negotiable)

$500

Home Inspection

$450-800

Termite/Pest Inspection (required by lender)

$125-150

Pool Inspection (if home has pool)

$150-200

HVAC Inspection (usually recommended on older homes)

$160-200

Total to Get Started

$4675–5450

PREPAIDS

Prorated Taxes

$2000

Prorated Home Owners Insurance

$2858.33

Pre-Paid Interest

819.86

Total Prepaids

$5678.19

CLOSING COSTS

Title Insurance (calculate) sometimes paid by the Seller

You may be able to negotiate for the Seller to pay part of the Closing Costs up to a certain percentage (read more), depending on the loan. This could reduce your total amount to buy a home by a few thousand dollars. However, in a HOT real estate market, most Sellers will not agree to this.

You need a PreApproval letter to start the home search phase in the home buying process in this area because:

You need to know exactly how much house you can afford and a lender is the best source for that information.

You won’t be able to make an offer on a home without a PreApproval letter, because they are almost always required by the Seller in this area.

I require this to ensure that you are not a “fraudster.”

I require this to “vet” you as part of my Safety Plan.

Here’s more…

Home sellers in our area will not (usually) accept an offer from a buyer unless it has a PreApproval letter with it. They don’t want to take their house off the market without some level of assurance that the buyer has lined up the financing for the home.

View My Video About This…

It may take several days or even a week to get a proper PreApproval letter. You will not (usually) have time to get one quickly, if we find a house you like and it’s in a multi-offer situation. So get PreApproved before you start looking at houses. You don’t want to “fall in love with a house” and then lose it because you weren’t prepared.

Plus, with all the scams and fraud that we real estate agents have to be on the lookout for, this is a typical “vetting” process that most high-quality, experienced agents require BEFORE working with a new home buyer. It’s kinda like a background check to ensure the buyer is “legit.”

And it’s also necessary for safety reasons. Believe it or not, showing empty houses to “strangers” is a dangerous proposition, and some agents have been MURDERED. So requiring a PreApproval letter is also a step to ensure my safety. 😉

You do not need to do a full loan application to get a preapproval letter, but it is more than just a quick phone call (like a prequalification).

Ask your lender to include a phrase in the letter that says your income, employment, and assets have been verified.

Items Needed To Apply for a Home Loan

After you find the right house and get it under contract, then you will need to fully apply for a home loan. Applying for a home loan these days is not for the “weak at heart”! It is a pain-in-the-neck process no matter how much money you have or which lender you choose. So mentally prepare yourself for a hassle, and you won’t be disappointed. ;-D

There is a lot of paperwork required in order to obtain a home loan. If a company is going to loan you hundreds of thousands of dollars, then they are going to want to know a lot about you and your ability to pay the loan back.

You will have to provide much of the paperwork multiple times throughout the loan process because of new lending standards (Dodd-Frank Wall Street Reform and Consumer Protection Act legislation and the Patriot Act).

Lenders are now required to verify certain items several times through the process…so please don’t get offended or frustrated when they ask you for something that you have already provided them.

Here’s what you will probably need to fully apply for a home loan (aka, mortgage):

Proof of identity for borrowers including driver’s license and Social Security number.

Address history for three years.

Copy of tax returns for past 2 years.

Banks names and numbers for all checking and savings accounts.

Bank statements for the past 3 months.

Documentation of all income including pay stubs for past 2 months.

Proof of bonuses for 2 years if applicable.

W-2 forms showing income for past 2 years.

Job history for past 2 years.

Net worth sheet with list of all assets and liabilities including account numbers.

Most recent 401K statements and other retirement accounts.

Copy of gift letter if applicable.

If self-employed, copy of balance sheet.

Divorce decrees if divorced in the past 2 years.

Proof of residency, if applicable.

College transcript if you were a student in the past 2 years.

Bankruptcy discharge papers, if applicable.

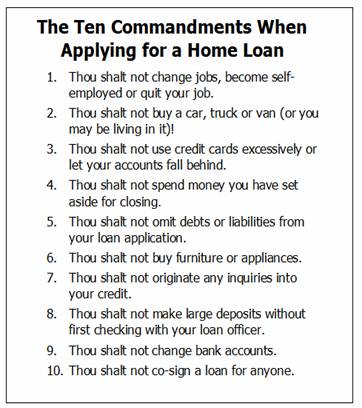

What Not To Do

Maybe you’ve just gotten married. Maybe you got a raise… or maybe you’re just plain sick of renting. Whatever the case, you’ve decided that it’s time to buy a house. You’ll be given all kinds of advice and pointers about what you should do and how you should do it, but there are things you shouldn’t do that are equally important when applying for a home loan.

Don’t be deceptive or dishonest when you’re filling out your loan application. Even if you get away with fudging the numbers a little to secure a higher loan (which is loan fraud), what’s the payoff you’re looking for? A monthly payment that you can’t truly afford?

Avoid moving your money around. To eliminate potential fraud and provide a degree of quality control, a lender will review the source of funds for your down payment and closing costs. Most likely, you will be asked to provide recent statements for any of your liquid assets. This includes checking accounts, savings accounts, money market funds, certificates of deposit, stocks, mutual funds, and even your 401K and retirement accounts. If you have been moving money between accounts during that time, there may be large deposits and withdrawals in some of them, which could make it more difficult for the lender to document properly.

Once you’ve been approved for a certain amount, resist the temptation to make any big purchases that could affect your ability to service the loan. Examples might be a new car, a boat, or expensive furnishings.

Sure you may be able to afford the mortgage and a car payment, but what if an unexpected expense comes along that causes your monthly budget to become unbalanced—you’ve got a shiny new car, but you may have trouble affording that and gasoline, and the mortgage, and the utilities. You’re caught in a situation where you’ve over-extended yourself. Even if you’re able to make it work on a month-to-month basis, you may have trouble putting money to your savings account.

Sometimes, knowing what not to do is just as important as knowing what to do.

Big Bank vs. Local Lender

At the risk of offending anyone who works for a big bank…

Many people think that using their current “big bank” as the mortgage lender will speed up the process because “everything is in one place.” That is not true; it is a myth. My understanding is that all lenders have access to the same databases and such. I have been told that using your bank will not change the process or make it easier.

A “big bank” is Chase, Bank of America, Wells Fargo, etc. They may be great banks but, that doesn’t necessarily mean they are great mortgage lenders.

Please understand that you can use whichever lender you want. I highly recommend that you shop around and talk to multiple local lenders and your local credit union (if you have one). Always keep in mind that, to a big bank, you are only one customer in a million. They don’t really have to care that much about you, because you won’t really impact their business. In contrast, to a small, local lender or credit union, you are one in a hundred (or thousand), and very important to their business. Plus, local lenders know the local laws and procedures. Big national banks don’t necessarily know how things work in Texas.

Another thing is experience. I highly recommend that you use a very experienced loan officer (aka, lender), which you can get at a local mortgage company. At a big bank, you may end up with a very inexperienced loan officer, in another state, who makes the process challenging, because he/she doesn’t know what they’re doing.

Plus, real estate agents don’t like big banks as lenders, because of delayed Closings. In a multi-offer situation, if you have a big bank as your lender, and another buyer has a local lender, the seller’s agent may highly recommend the other buyer. I’ve had listing agents tell me they won’t accept an offer from a buyer using a big bank! (This has happened multiple times.) So always remember that the lender you use, is part of your competitive advantage.

When you have deadlines to meet, and your movers are scheduled to pick up your belongings, and you will have no place to live if you don’t Close on time, then the stress of a delayed Closing is very real. Big banks are notorious for delayed Closings. If you miss your Closing date, you could lose your 1% earnest money, but there are no consequences for the lender.

I’ve had several clients over the years, who didn’t listen to me, used their big bank, and had horrible experiences. I’ve had multiple clients call me crying, the week before Closing, due to all the issues with their big bank lender and a delayed Closing. I had a horrible experience once, when a Wells Fargo loan officer demanded that my client leave her mother’s deathbed to perform a task, and the bank STILL didn’t Close the deal…and my client’s mother died while she was away. (I closed my Wells Fargo account over that! Absolutely horrible experience.) Unfortunately, there’s nothing that I can do to help, the week before Closing, if you used a big bank lender. So I try to warn my clients in advance, to try to prevent these sad and stressful scenarios.

To be fair, I have seen a handful of deals, with big bank lenders, that went very well. However, several of them were for employees of the bank…who had the “insider advantage.”

Lenders to Consider

If your employer offers a credit union, then check with it first. Plus, here is a list of lenders (loan officers) that my clients have recommended to me:

Will Swallen

Radiant Mortgage

Phone: 713.428.2155

www.williamswallen.com

David Krichmar

DaveYourMortgageGuy.com

Dave@DaveYourMortgageGuy.com

832-689-6012

Want to know how to hire the best Katy real estate agent? See below!

NOTE: Many of these items are specific to Texas agents.

___ Did your agent give you the “Information About Brokerage Services” notice that is legally required by the Texas Real Estate Commission before showing you houses? Can your agent effectively explain it?

___ Did your agent provide all the other necessary disclosures, notices, and the Buyer’s Representation Agreement to you before showing you houses? Be careful! You don’t want to find out after-the-fact that your agent actually represents the Seller.

___ Can your agent effectively explain the HOA maintenance fees, MUD and LID taxes, compliance certificate requirements, amenities, property tax rates, school performance ratings, and other important information for the neighborhoods you are looking at?

___ Does your agent know how to provide you with an accurate CMA (price analysis) on a home before you make an offer? Is he or she committed to helping you get the right price or does the agent just want you to buy the highest priced home you can afford? (See “How to Price a Home Correctly“)

___ Does your agent point out possible defects of homes when you tour them or does your agent always seem to overlook the obvious problems of a home and try to convince you that they don’t matter? (Check my client satisfaction rating.)

___ Does your agent actually show you homes or does he or she expect you to drive the neighborhood on your own and then contact the listing agent directly to let you see the house? A dedicated agent wants to be with you every step of the way.

___ Has your agent set up a customized automatic home search for you that is pulled directly form the local MLS? Or are you still trying to find homes on your own using the limited online search Websites available in your area? These programs (such as Realtor.com, Zillow, Trulia, and Homes.com) can be outdated very quickly showing contract-pending homes as “active.”

___ Does your agent use an online paperwork system where you can e-sign documents instead of having to fax and scan them (which is sometimes challenging and time-consuming)? What if your spouse is still back home in another state or country? You need to be able to e-sign!

___ Does your agent work to negotiate a residential service contract (aka, home warranty) in the deal or provide one for you to protect you from too many future home repairs?

___ Does your agent have at least a 4.5 star client satisfaction rating with the local board of area Realtors? What’s your agent’s YELP rating, Homes.com endorsements, Angie’s List reviews, and so on?

___ Does your agent have 20 years experience? (Trick question.) IT DOESN’T NECESSARILY MATTER! There are terrible agents with 30+ years of experience who even have a broker’s license. And there are outstanding agents with only a couple of years experience. Time does not equal quality in this business. Time cannot guarantee attitude, dedication, integrity, intelligence, or commitment to customer service. Check their satisfaction rating...this is a free service for all members of the Houston Association of Realtors (HAR). If your agent hasn’t signed up, maybe they have something to hide.

“If you’re not sure whether you need a real estate agent or not, please take a look at Do I Need a Real Estate Agent to help you decide.”

RECOMMENDATION: Change video Quality setting to 1080p.

If you are buying a home in Texas, then you need to learn about the home buying process, which may be different than other states. One thing to consider is that before you even begin the process of searching for a home, you must:

Determine how much house you can afford. A lender is the best place to get that information…it is part of the pre-qualification process.

Determine if you will actually qualify for a loan. Some good people don’t, under today’s stricter lending guidelines. You will need a pre-approval letter from a lender to submit with an offer on a home in Katy….Seller’s almost always require one these days!

Determine how much it will cost to buy a home. Do you have enough money on hand for the earnest money, option fee, down payment, closing costs, inspections, fees, etc?

The following video explains the home buying process (and Option periods) in the Katy Texas area…so you know what to expect and how things are in the Lone Star State.

This information about buyer representation in Texas is so important that the Texas Real Estate Commission REQUIRES that we discuss this before seeing houses.

Click image above to see entire document

Things Are Different in 2024!

There are BIG changes hitting the entire real estate industry as of August 2024, so make sure you watch my videos to understand those changes and how they will impact you.

RECOMMENDATION: Change the video Quality setting to 720p. You can also change the Playback Speed.

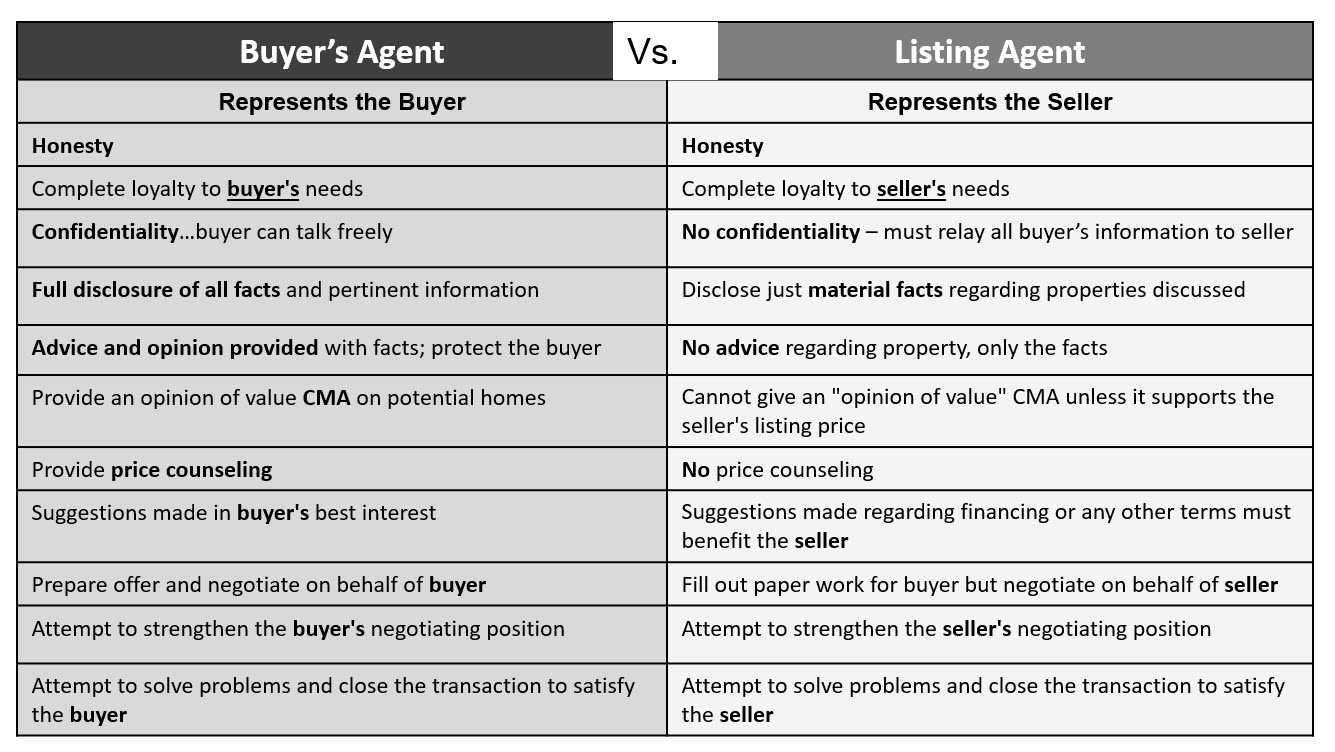

Buyer’s Agent vs Listing Agent

There are different rules for how a Buyer’s Agent can work with a home buyer vs. how a Listing Agent can work with a home buyer.

How Can I Make Sure My Agent is On My Side?

As you can see, if you want all the pertinent information available to make the best buying decisions, then it is important that you obtain your own representation with a Buyer’s Agent. Having a Buyer’s Representation Agreement benefits you by:

Protecting your confidentiality

Allowing me to provide you with all the information at my disposal, including advice on the price

Allowing me to negotiate based on your best interests

Giving you a partner who is loyal to you

List of My Value-Added Services for VIP Home Buyers

My job isn’t “just” helping you find a house to buy…I’m helping you through the entire 2-4+ month process of buying a home. There are over 100 action items on my checklist during the purchasing process. I’m looking out for you every step of the way and keeping my eye on the listing agent, the seller, the builder (if applicable), the lender, the inspector, appraiser, HOA, and the title company. I’m on YOUR side because I’m YOUR agent and have a fiduciary duty to take care of you to the best of my abilities.

I help with house pricing data/analysis, contract negotiations, legal paperwork and deadlines, inspections, appraisal issues, repair negotiations, home warranties, HOA issues, hazard insurance, surveys, title insurance, home warranties, and more. I have the expertise to help solve complicated problems that often occur in the transaction and I work to prevent, to the best of my abilities, you losing your earnest money or worse.

My goal is to make the process as easy as possible and to guide you every step of the way. You’re not trained in all the legal deadlines and requirements regarding Texas real estate, but I am! Real estate is a huge financial and legal commitment. Don’t you deserve to have a Five Star real estate agent on your side?

Premium, customized home search (based on my knowledge of the area school ratings and flood zones) to filter out homes that don’t meet your criteria. You can’t get this level of a home search on your own!

Online home review BEFORE you tour a house, to look for potential defects such as high-risk flood zone, high-voltage power lines, MUD tanks, previous flooding, and other issues…so you don’t waste time touring undesirable homes.

Detailed home tours (in-person or via VIDEO* for out-of-town clients), where I help identify the features and benefits of each home and neighborhood as well as any potential home defects (so you don’t end up with a “money pit”).

*I’ve sold many homes “sight unseen” to out-of-state an out-of-country clients, via my HD video walkthroughs (view sample). I will even video the inspector summary and final walkthrough for you.

Hyperlocal knowledge and expertise so I can point out the amenities, PROs and CONs, and HOA details of most neighborhoods in this area.

“Sheila’s Home Buyer Guide” for THIS AREA (not generic) that includes helpful info about the INs and OUTs of the home buying process here in Texas. Remember that real estate laws are different from state to state.

Detailed pricing data and expert Comparative Market Analysis (CMA) on the house you select to purchase, so you can make a good decision regarding the price. Pricing homes is my superpower! 😊

Expert contract creation and negotiations to help you get the house you want…even in multi-offer situations.

Assistance with hiring home inspectors, reviewing inspection reports, and guiding you on necessary repairs/costs so you make the wisest decision.

Floorplans! I can create a floorplan of any home you purchase, whether provided by the home seller or not.

Project management of all the legal deadlines and requirements throughout the transaction. You’ve got enough to deal with the packing, moving, and job/school relocation activities!

Assistance in managing the title commitment/insurance process and working with the title company.

Assistance with home surveys and their impact on your transaction.

Assistance with appraisals and their impact on your transaction. I know how to protect you if the appraisal “comes in low” (which can happen in super-hot seller markets).

Assistance with HOA compliance documents, fees, and procedures.

Help with obtaining home owner’s insurance and flood insurance.

Guidance with choosing a home warranty as needed.

Helpful information regarding all the utilities (MUD info) applicable to the home you purchase.

Helpful “Planning the Move” information and “Info About New Home” that will help make your transition easier.

“Moving Survival Kit” provided as my Closing gift. This contains the things you will need on your moving day (but are usually packed) such as: soap, trash bags, paper plates, cups, toilet paper, snacks, box cutter, etc.

Guidance on your homestead tax exemption and how to apply for it in a timely manner to reduce your property taxes.

Helpful monthly home maintenance reminders, to take care of your investment!

Whew! That’s way more than “just” showing houses. 😄

Here are some other articles about “buyer representation”…

But I’m Buying From a Home Builder – So I Don’t Need An Agent

A home builder is a seller…so you still need your own representation! Believe me when I tell you, that sales rep sitting at the builder’s model home may be a super-nice guy or gal, but he/she is paid to look out for the builder’s best interest, not yours.

The builder’s sales agent is not going to tell you that they are building in a high-risk 100-yr flood zone, or that there is a landfill or prison a half-mile away from the neighborhood or that the specific schools zoned to the neighborhood are low-performing (notice how they talk about the school district?), or that the neighborhood is struggling to sell homes (and home values are falling). The builder’s agent will not tell you that the last three buyers who bought the same floorplan that you want, paid $30,000 less than the price he or she is showing you now…but I will! What’s more, the sales agent will show you that the house originally listed for $100K more than current list price to make it sound like a great deal.

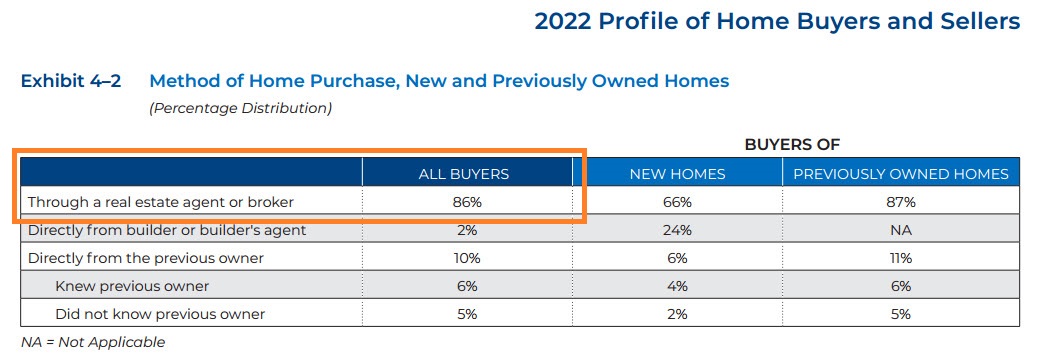

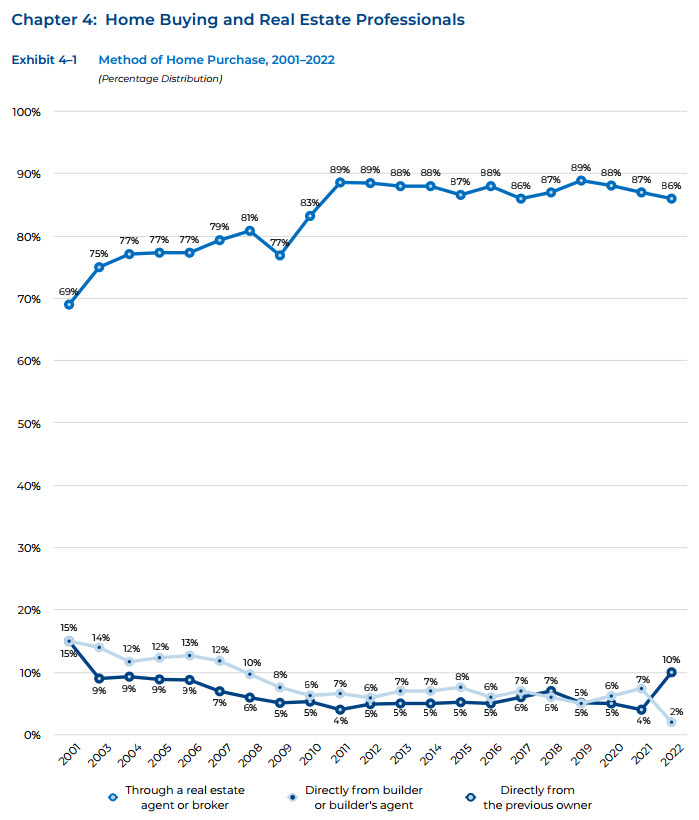

By the way, the number of home buyers buying directly from a builder or builder’s agent is only 2 percent. Whereas 86 percent of home buyers choose to do so through are real estate agent or broker (see below).

Source: National Association of Realtors Profile of Home Buyers and Sellers

Please know that you are not necessarily going to save money by not having your own agent.

And always remember that you still need a home inspector when you buy a new-construction home. The builder’s inspection process is not for your protection…it is just part of their system. In my experience, new homes typically have longer inspection reports (more stuff to fix) than good-condition resale homes because the “kinks” haven’t been worked out yet…by the first owner.

Once you have a Buyer’s Representation Agreement in place, you should always state that up front to builder’s sales agents (if touring new home models) because, by law, they need to know that you have representation.

Does My Real Estate Agent Represent Me or the Seller?

When I bought my first house in the mid 1990s, Texas was kind of a “Buyer Beware” state. In fact, a home Buyer could spend weeks looking for a home with a real estate agent, telling her secret information (like how much you were willing to pay for a house), not knowing that everything you told that real estate agent would be told to the Seller because the real estate agent was actually representing the Seller–not you (the Buyer)!

Here’s what you need to know…

Things Are Different in 2024!

There are BIG changes hitting the entire real estate industry as of August 2024, so make sure you watch my videos to understand those changes and how they will impact you.

RECOMMENDATION: Change the video Quality setting to 1080p. You can also change the Playback Speed.

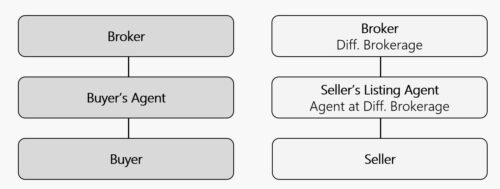

Agency Relationships in Texas

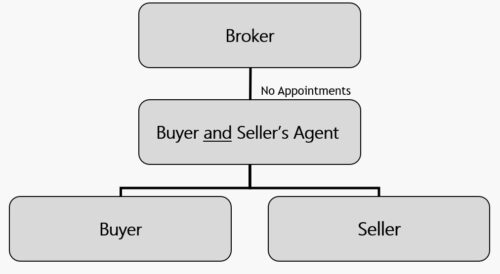

Another fact that you need to know is that Texas is a dual-agency state…meaning that a real estate broker (such as Keller Williams Signature) can represent both the Buyer (you) and the Seller (them) in a the same transaction. This is called “intermediary agency.” These visual aids will help you to understand…

Typical Agency

In this case, you are represented by one broker while buying a house listed by another broker.

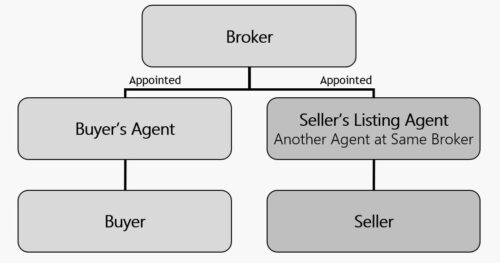

Intermediary Agency With Appointments

In this case, one broker is representing both you and the Seller…because the house that you are buying is listed with the same broker, but with a different agent. However, you have an appointed agent (Sheila Cox) and the Seller has an appointed agent (Unknown) and both agents have to maintain their fiduciary duties including confidentiality. So I am not allowed to share your private information with the other agent. This situation may occur frequently with large brokerages who have lots of listings.

Intermediary Agency WithOUT Appointments

This situation may only occur if both the Seller and the Buyer agree to it in writing. In this situation, you are buying a house that I have listed for one of my other clients. I would be representing both you and the Seller, so my fiduciary responsibilities would be limited. Frankly, I don’t work these types of deals. If you wanted to buy one of my listings, then I would step back and find another real estate agent to be your appointed agent…so you would still have full representation.

Now you need to understand two more important things:

“That’s what I used to think! In fact, before I became a licensed real estate agent, I did several FSBO (For Sale By Owner) sales and THOUGHT I knew what I was doing. But if I had known then what I know now…I never would have risked it. Here’s what I’ve learned…” –Sheila Cox

Yes…You Need a Partner During the Home Buying Process!

Your home is probably your largest single financial investment. Most homes in my area (Katy and Sugar Land TX) cost over $200,000. If you had a $200K legal problem would you try to handle it yourself or would you high a quality attorney to help you?

Of course, not all attorneys are equal in skills, knowledge, integrity, experience–and neither are all real estate agents. In fact, most people have had at least one bad experience with a low-quality real estate agent. I know I have! As in any industry, please consider that it is possible the 80-20 rule applies to real estate agents…maybe 20 percent are not very highly qualified, but that would leave another 80 percent who are! (Just like in your line of work…do all your peers provide the same quality of expertise?) Always keep in mind that having a bad experience with one agent, doesn’t mean that all real estate agents are bad. The trick is finding and hiring the right, high-quality agent. Here are some things to consider…

Real Estate Laws Vary From State to State

Not all states have the same real estate laws. In fact, Texas real estate laws and practices are highly unique in comparison to other states. Just because you have bought or sold a home in another state, does not necessarily make you qualified to do so in Texas. (I know, I know…we Texans think everything is bigger and better here!) But the fact is, Texas real estate is so complicated, that agents are required to have many more hours of education to get a license here than any other state…about three times more hours of education than average across other states!

Your Legal Exposure in a Real Estate Transaction Can Be Very High

A very common type of real estate lawsuit involves Deceptive Trade Practices in which a home buyer accuses the home seller for not properly disclosing the actual condition of the property. In these cases, treble damages (three times the actual cost) can be awarded. This can really add up! And the cost for hiring a real estate attorney to defend yourself can cost well over $10,000! It doesn’t always matter that you did nothing wrong. Without a licensed real estate agent there to watch out for your interests and to make sure that you comply with all of the Texas real estate code and statutes, you can end up with a real nightmare on your hands.

Likewise, home owners can sue home buyers for non-performance or can keep large amounts of earnest money if a contract doesn’t Close. This is when you want a professional agent looking out for your best interest to (hopefully) prevent you from breaching a contract and losing your earnest money. And if a lawsuit is not prevented, isn’t it best to have a large, reputable real estate brokerage (and their legal team) behind you when you need it?

Real Estate Data Is Not a Matter of Public Record In Texas

Texas is one of 14 non-disclose or partially-disclose states in the U.S. That means that real estate sales prices are not a matter of public record in Texas. So Internet-based companies like Zillow and Trulia do not have the real data to accurately “Zestimate” what a house is worth in our state. Property tax records are what these companies use in order to estimate a home’s value. But everyone in Texas knows that tax appraisal values do not usually reflect the actual value of a home…they are typically lower than actual value. (Which helps to keep the costs of our already too-high property taxes down.)

The only people in Texas who have accurate sales records are members of the Multiple Listing Service (MLS) including real estate agents and home appraisers. So if you want an accurate sales price analysis on a home (so that you don’t pay too much for it) you will need to hire one of these professionals.

CAUTION: Not all real estate agents are equally good at sales price analysis. Hire an agent who knows how to put together a valid comparative market analysis (CMA).

Do You Really Want (or Have the Time) To Learn Everything You Need To Know About Real Estate?

Yes, you can read up on real estate and I encourage you to do so. But no amount of book-learning is going to make up for the actual real-world experience a high-quality real estate agent offers. Real estate laws change yearly and vary from state-to-state. So most books are out-of-date by the time they go to print or are too generic to meet your specific state’s requirements.

And please don’t believe all the real estate advice that you can read on the Internet. I recently read an Internet article about how to sell a home without a real estate agent and most of the advice offered was not accurate according to Texas real estate laws…which could get you into some costly legal trouble.

Besides all this…aren’t you busy enough with just deciding on a home, getting your lender all the necessary paperwork, planning the move, changing utilities, registering at new schools, packing, training for the new job, and so forth?

It’s Complicated! Are You Qualified to Manage the Entire Transaction?

A high-quality real estate agent wears many hats: local area expert, state real estate rules expert, amateur remodeler, price analyzer and mathematician, home decorator/stager, professional photographer and videographer, marketing expert, chauffer and tour guide, psychologist, marriage counselor, sales negotiator, amateur home inspector, administrative assistant, project/transaction manager, communications expert, and tech writer. Very few professions require skills in so many different areas! I don’t think the average person realizes how much they expect their real estate agent to handle.

And then there are the home buyers who think real estate agents just help them find a home to buy and once the contract is accepted, their job is over; but that’s just the “end of the beginning” for an agent! Likewise, a great listing agent doesn’t just take a few photos, put a sign in the yard, and wait for the offers. A great real estate agent is looking out for you every step of the way and keeping their eye on the other agent, the other party (buyer, seller, builder), the lender, the inspector, and the title company.

Here are more examples of what a real estate agent does for you:

Helping you maneuver the Option Period, including getting the right inspections and, if necessary, repair estimates. Do you know how to “exercise your option” properly if needed? Do you know how to minimize the impact of the OP when marketing a home as a seller? How do you deal with lender-required repairs?

Negotiating necessary repairs with the Seller so you don’t get stuck with them after Closing. Can you get repair estimates in a timely manner? Do you know how to effectively overcome common repair objections? Do you have the knowledge needed to accurately estimate a remodeling project?

Helping you meet your contractual obligations (such as appraisals, surveys, deed restrictions, HOA compliance certificates, legally required disclosures, title commitments, hazard insurance, and more) in a timely manner so you don’t find yourself in breach of contract. How many days do you have to get the survey? If there is an existing survey, what other legal document is required? What do you do if encumbrances are found in the title search? What do you do if your financing falls through after the deadline in your contract?

Dealing with home inspectors, appraisers, lenders, and title companies to get them to do their jobs in a timely manner so you can move when you plan to. There are many moving parts in a real estate transaction! What do you do if the lender doesn’t get the paperwork to the title company on time? How do you know if the fees on the HUD1 are accurate? Did you remember to get hazard insurance and order the residential service contract? Did you negotiate a temporary lease so you can move out after Closing? What do you do if the Closing falls through?

Do You Know the Area As Well As You Need To?

If you are moving to a new area, there is no substitute for getting the opinions and advice of a local real estate expert. Even if you know someone who lives in the area that you are moving to…they only see that area from their individual, and probably limited, perspective. You really need a professional who has the BIG picture and the “inside information” that only a local real estate expert can provide. Someone who will listen to your specific needs and find the right neighborhood and right home for you.

And watch out for online companies offering you price reports and other types of statistics based on ZIP Codes. Sugar Land consists of multiple ZIP Codes and let me assure you that a price analysis for a home in Sweetwater in 77479 is not going to accurately reflect the price of a home located in Woodstream which is in the same ZIP Code.

Home prices vary not only from neighborhood to neighborhood, but even within the same neighborhood. For example, a home in New Territory that has a water view is going to be valued higher than a home right down the street that does not have a water view. And a 2000-2600sf home probably has a different average sales price/sf than a 3500-4100sf home…even on the same street. AND those same values can change from month to month (depending on the actual figures for recently closed home sales). Do you have the real sales data and price analysis expertise to ensure that you don’t pay too much for a home or list it at an unrealistic price?

Sometimes You Need An Objective Partner When Choosing the Right Home

Let’s face it…even the most level-headed, objective, analytical engineer-type can get emotional (and become unobjective) about a home. Trust me on this observation! Everyone gets emotional on some level about the house they are going to live-in for the next several years. And if you have raised four kids, two dogs, and three cats in a home for the past 23 years…forget about it. You may not see the worn-out carpet and outdated wallpaper for the good memories.

Sometimes it is just like “love at first sight” when buying a home. And that emotional response to a home may cause you to do something you will regret later. You need an unattached, neutral, third-party (such as a dedicated real estate agent) to help keep you focused on the facts and the big picture. I’m not saying all agents do this. I agree that some agents are just out to close the deal no matter what, and don’t really care if you are going to end up with a poor investment that you will regret when resale time comes along.

But I once talked a client out of a $650,000 home because, when I was researching the home and looked at the bird’s eye view, I found a hidden dump where you could see railroad cars deteriorating and rusting into the local water supply! You never would have seen this driving around the neighborhood because it was hidden behind fences and shrubbery. But when I showed my clients what they would be living next to, even though they were disappointed because they loved the house, they were thankful that I found the problem and objectively pointed it out to them before they purchased that potentially costly mistake. I ended up selling them a $525K home they loved and we are very good friends to this date because they know I am trustworthy and not just looking out for the highest sales commission I can get.

List of My Valuable Services for Home Buyers

My job isn’t “just” helping you find a house to buy…I’m helping you through the entire 2-4 month process of buying a home. There are over 100 tasks that I perform during the purchasing process. I’m looking out for you every step of the way and keeping my eye on the listing agent, the seller, the builder (if applicable), the lender, the inspector, appraiser, HOA, and the title company. I’m on YOUR side because I’m YOUR agent.

I help with price analysis, contract negotiations, legal paperwork, inspections, appraisal issues, repair negotiations, home warranties, HOA compliance inspections, hazard insurance, surveys, title commitment, home warranties, and more. I have the expertise to help solve complicated problems that often occur in the process and I work to make sure that you don’t lose your earnest money or worse.

Real estate is a huge financial and legal commitment. Don’t you deserve to have a Five-Star real estate agent on your side?

Here’s How I Add Value to Your Home Buying Process:

Premium, customized home search (based on my knowledge of the area school ratings and flood zones) to filter out homes that don’t meet your criteria. PLUS, my search has the “Coming Soon” listings not available on Zillow, RedFin, etc. You can’t get this level of a home search on your own!

Online home review BEFORE you tour a house, to look for potential defects such as high-risk flood zone, high-voltage power lines, MUD tanks, previous flooding, and other issues…so you don’t waste time touring undesirable homes.

Detailed home tours (in-person or via VIDEO* for out-of-town clients), where I help identify the features and benefits of each home and neighborhood as well as any potential home defects (so you don’t end up with a “money pit”).

*I’ve sold many homes “sight unseen” to out-of-state an out-of-country clients, via my HD video walkthroughs (view sample). I will even video the inspector summary and final walkthrough for you.

Hyperlocal knowledge and expertise so I can point out the amenities, PROs and CONs, and HOA details of most neighborhoods in this area.

“Sheila’s Home Buyer Guide” for THIS AREA (not generic) that includes helpful info about the INs and OUTs of the home buying process here in Texas. Remember that real estate laws are different from state to state.

Detailed pricing data and expert Comparative Market Analysis (CMA) on the house you select to purchase, so you can make a good decision regarding the price. Pricing homes is my superpower! 😊

Expert contract creation and negotiations to help you get the house you want…even in multi-offer situations.

Assistance with hiring home inspectors, reviewing inspection reports, and guiding you on necessary repairs/costs so you make the wisest decision.