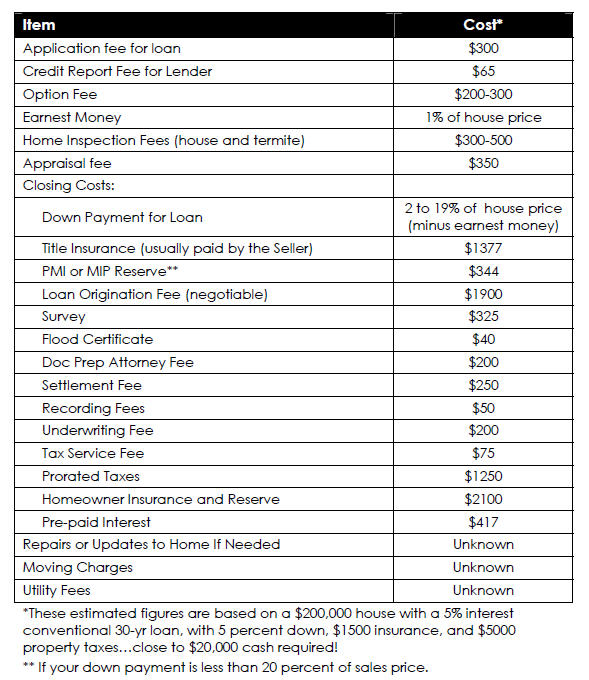

Newcomers this to area always ask me, “What is a MUD?”

In most parts of Fort Bend County, neighborhood infrastructure is provided through a Municipal Utility District, commonly called a MUD. A MUD is a special-purpose local government entity created under Texas law to finance, build, and maintain essential utilities for a specific area—usually a residential community.

When a new subdivision is developed, the developer often forms a MUD to fund infrastructure such as water lines, sewer systems, drainage facilities, and sometimes roads, parks, or recreational amenities. Instead of the developer paying the full cost upfront, the MUD issues bonds to build these improvements. Those bonds are then repaid over time through property taxes collected from homeowners within the district.

For homeowners, this means that your property tax bill will typically include a separate MUD tax rate in addition to county, school district, and other local taxes. The MUD uses those tax revenues to repay infrastructure bonds and operate the district’s utilities. With a MUD you will have a monthly bill that covers your water, sewer, and trash service. In addition to that, your property taxes will include a portion that goes to the MUD. So they do add to your property tax bill.

#image_title

A MUD is governed by a board of directors, usually elected by residents who live within the district. This board makes decisions about budgets, tax rates, and ongoing infrastructure maintenance.

MUDs are very common in fast-growing suburban areas like Fort Bend County because they allow new communities to develop without requiring existing taxpayers in nearby cities to fund the infrastructure. There are PROs and CONs of having MUDs to provide utilities, but regardless of our opinions on them, you will be hard-pressed to find many neighborhoods in this area that are not assigned to a MUD.

There are a few things that we need to do before we can start touring houses. The Texas Real Estate Commission, National Association of Realtors, and my broker require that I go over certain information with you FIRST.

Five Steps to Get Started

Here are the required steps…

NOTE: There were some BIG changes that affected the entire U.S. real estate industry as of August 2024, so you MUST get up-to-date by watching my videos. We are no longer allowed to show houses to you unless you have a written agreement in place. You can also view a summary here.

Please watch my video about Agency & Representation so you understand what it is. This is very important information! Call me if you have any questions.

RECOMMENDATION: Change the video Quality settings to 720 and remember you can change the Playback Speed as well.

Also view my video about Buyer’s Agent Compensation so you understand the three different ways that buyer’s agents are compensated in today’s real estate industry. Call me if you have any questions.

RECOMMENDATION: Change the video Quality settings to 720 and remember you can change the Playback Speed as well.

Please email me (scox@katyhomesforsaletx.com) a copy of your PreApproval letter from your lender. You can see my video about why we need this now here. If you don’t have a PreApproval letter yet, please read this article (which also has a list of some lenders you can contact).

Alsoemail me your current address and full legal names so I can create the necessary paperwork to get started including:

Other required buyer disclosures (as required in Texas)

E-sign the documents that I send to you via a program called DotLoop. This is an easy way to e-sign documents online.

Once we complete these five steps I can start touring homes with you either in person or via my online video tours! I can’t wait to help you buy a GREAT home in my wonderful area!

by Sheila Cox, Five Star Realtor | Updated April 2026

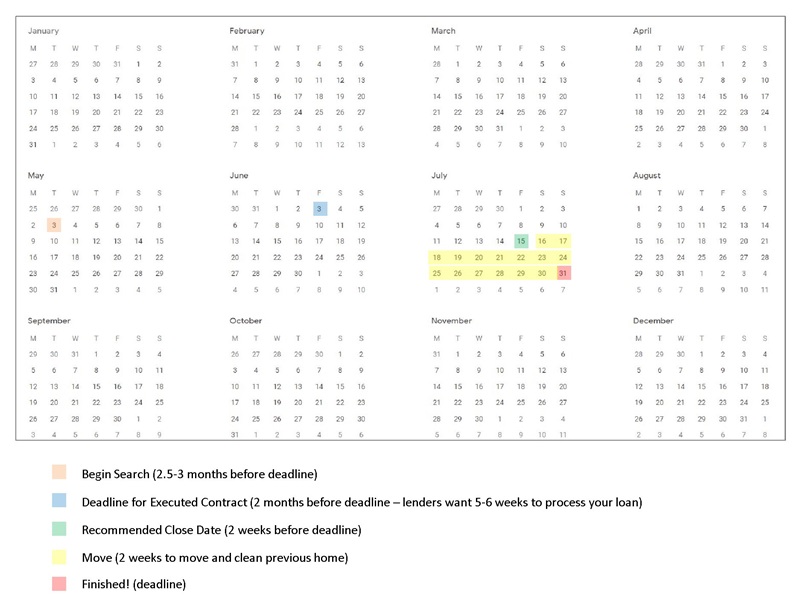

One thing I’ve found as a real estate agent: most people need help with their home buying timeline. So my recommendations are listed below.

Home Buying Timeline for a Resale Home

Start with a Deadline. That’s the date you absolutely have to be out of your current home/apartment. This Deadline may be the end of a lease or a move-out date for an existing home that you are selling.

Begin Search. You should begin your search approximately 2.5 to 3 months before your deadline. Keep in mind that most home owners will want you to Close within 5-6 weeks of executing a contract because that’s the typical time it takes for a lender to process your loan. It may take several weeks before you find a home and get an accepted contract. Some people start their search even earlier, to have more cushion, but they must be prepared to Close early and pay two house payments until the end of their current lease or move out date on current home. (Actually, you don’t usually begin paying a new mortgage for at least one month after Closing. So if you Close in the middle of June, your first house payment may not be until August 1.)

Deadline for Executed Contract. You must be “under contract” on your new home at least 6 weeks before your deadline but 8 weeks is preferred. Again…this is to allow time for your lender to process the loan (usually 5-6 weeks). You should allow a 2 week gap between Closing on your new home and moving out of your current home in order to give yourself time to pack, move, and clean. NEVER plan to Close and move out on the same day. Closings don’t always happen on time, as scheduled. There can be delays caused by the lender. You do not want your belongings on a moving van before you have a definite place to put them!

Recommended Close Date. You should Close on your new home about 2 weeks before your Deadline to move out of your existing home. However, this will need to be negotiated with the Seller of the new home. If they have already vacated the property, they will want a quick/short Closing date. If they are still living in the home, they may want a longer date before Closing or they may want a Temporary Lease to live in the home, after Closing, to have time to pack and move.

Home Buying Timeline for a New Construction Home

This timeline is for purchasing a resale home. If you are buying new construction (home being built from “dirt”) then it will take 5-6 months or more. Keep in mind that there are sometimes material shortages and supply-chain issues, and some home builders have delays. Rainy weather can also delay a Closing date for new construction homes.

In a hot real estate market, where homes are getting multiple offers within a few days of being listed, you need to know how to make your offer to purchase a home more competitive. The more you want the home, the more competitive you will want to make the offer.

Please view my detailed video (50 mins) to learn about our Texas contracts and addendum. You should do this in advance so you are prepared in case we have to write an offer in a hurry. You can download and print the sample docs (which we go through in the video). Please write down your questions, so we can discuss them.

The video and sample docs are exclusive to clients only…so sign up!

In my video I explain the following items and more.

Contract Item

Comment

Estimated Cost*

Sales Price

The higher the sales price, the better your offer.

You usually have to offer over list price to win in a multi-offer situation.

Termination Option

NOTE: Relocation companies do not allow Termination Options (which are unique to Texas).

Negotiable for 7-10 days and $200-500 fee. Waiving your Termination Option can be a good way to be competitive, and you are still allowed to do inspections. However, you will have little negotiating room for repair requests. In a hot real estate market, most sellers won’t agree to repair requests anyway. (See more about inspections and common issues on homes in this area.)

If you want a Termination Option, but you also want to be competitive, then offer a $1000 fee to show that you are a serious buyer. If you do not “exercise your option to terminate” then your Option fee is applied (credited) to your Sales Price at Closing.

$200-1000

Requested Non-Realty Items

Do not request excluded items if you want to be competitive.

You can ask for appliances, furniture, etc. and offer to pay for them in a Non-Realty Items Addendum.

$10 or more

Title Policy

Sellers usually pay for the title policy but you should pay for it if you want to be super-competitive.

Buyers usually pay for a new survey if the sellers do not have an accurate one available.

$425 at Closing

Home Warranty

The Seller usually pays for a Home Warranty, but the Buyer chooses which home warranty company and policy type they want, and the title company orders it and pays for it out of Closing funds.

To be more competitive, pay for the Home Warranty yourself.

$500-800 (with pool)

Closing Date

If the home is vacant, then the sooner the better to Close (for the Seller). Being flexible on a Closing date, to match what the Seller wants, can be a good way to be competitive. Closing time frames are mostly determined by the lender who usually require 5-6 weeks. Cash buyers can usually close in 3-4 weeks as long as their funds are readily available.

Possession/Temporary Lease Backs

If the home is still occupied by the owner, then offering a Temporary Lease Back to the Seller, so they have time to pack and move after the Closing, can be a good way to be competitive.

Seller’s Contribution to Closing Costs

If you need help with Closing costs, because you do not have a lot of cash available for the purchase, then your offer will not be very competitive. Asking the Seller to pay for anything extra lowers their “net proceeds” from this transaction.

Sometimes you can offset “Seller’s Contribution to Closing Costs” with a higher sales price, but not often in a multi-offer situation.

Type of Financing

A conventional loan from a reputable local lender will make your offer more competitive. If you have a big bank (such as BofA, Wells Fargo, or Chase) then you will not be as competitive (because listing agents don’t like them due to Closing issues).

FHA loans are not competitive because of the stringent inspection process and reputation for low appraisals.

Days for Buyer Approval

On the Third Party Financing Addendum, we typically put 21 days for Buyer Approval, but if you have all your paperwork turned into the lender, and your lender says it’s OK, then you may want to put 14 days to shorten this contingency (to be more competitive).

Appraisal Addendum

If you are bidding high on a house and have concerns that it will not appraise, then you should request an Appraisal Addendum (see my detailed article and video about this). This is especially true if you are a cash-rich buyer. However, this makes your offer less competitive than offers who do not make this request.

If you can afford it, do not request an Appraisal Addendum and be prepared to pay the difference between the sales price and the appraised price (plus down payment and Closing costs).

Subdivision Info

You can usually get the deed restrictions for a neighborhood online. If you want a printed copy, then you may be charged for it and you will have to request it on the HOA addendum. This is very unusual and will make your offer less competitive.

Cost Varies

$300-500

HOA Transfer Fee

The transfer fee should be listed on the MLS, but it may be inaccurate. The Buyer usually pays the transfer fee. There may be other fees $200-400 approximate) charged by the HOA before Closing…each HOA is different.

Cost Varies

$200-400

Foundation Fee

Johnson Development who runs Cross Creek Ranch, Sienna Plantation, and Riverstone, requires that Buyers pay an extra fee at Closing, usually equal to one year’s HOA maintenance fee. There may be other neighborhoods/developers that require this as well. Make sure you identify “who pays what” in the contract.

Usually equal to HOA fee $1100-1300

Capitalization Fee

Johnson Development who runs Cross Creek Ranch, Sienna Plantation, and Riverstone, requires that Sellers pay an extra fee at Closing, usually equal to .25% of sales price. There may be other neighborhoods/developers that require this as well. Make sure you identify “who pays what” in the contract.

Cost Varies but usually .25% of sales price

*All of the costs listed are ESTIMATES only.

To write an offer to purchase a home, I will need the following information:

Full Legal Names (both people): __________________________ and ______________________________

Separate email addresses for each of you: __________________________ and ______________________________

(for e-signature system to be legal, they require separate emails)

Sales Price: $____________

Down payment: $___________ or ____%

Loan Type: Conventional

Loan Duration: _____ years

Loan Interest Rate: ____%

(The rate should be “worst case” scenario, in case you want to use this as a reason to back out of the deal due to financing issues.)

Closing Date: _________________

Current Address: _________________________

Items to include in Non-Realty Items Addendum: Refrigerator?, W&D?

Special permission to do stucco inspection or hydrostatic testing (very uncommon here)

One troublesome aspect of home buying and selling is how to handle low real estate appraisals.

A real estate appraisal is an estimate of the market value of a piece of real estate based upon a variety of factors.

In the definition above, notice the word ESTIMATE. If you ask five different appraisers to give you an appraisal for one home, you will end up with five different prices/values. So never consider an appraisal to be absolutely true, objective, and infallible—it’s an OPINION only. It’s not like 2 + 2 = 4. It’s more like the appraiser chooses the comparable homes (“comps”) and adjustment numbers he wants, to make the home equal to the sales price or less…depending (in my opinion) on how much down payment the buyer is paying.

I’ve seen overpriced houses appraise for the sales price and I’ve seen fairly priced homes NOT appraise for value. What’s the difference? I think at least part of it is how much the buyer is putting down on the home (but I can’t prove that). In my experience, it’s interesting how often homes appraise when the buyer is putting 20 percent down, and how often the appraisal “comes in low” when the buyer is only putting 3 to 5 percent down.

I’m a very analytical real estate agent, so I actually review all appraisals that I receive, to see what the appraiser did and how he valued the property. One thing that has always amazed me is how rarely appraisers choose true comparables to the subject home. We’re supposed to choose 3-5 homes sold in the past 6 months that are as near the subject property in size, quality, age, amenities, and proximity as possible. But I’ve seen an appraiser go back a year to find the lowest comps possible, when there are plenty of comps that are within the 6-month preferred window. I’ve seen appraisers use comps in totally different neighborhoods, zoned to different schools and with different amenities, rather than use the comps available in the same neighborhood. I’ve seen appraisers use homes that where larger or smaller than our +/-300sf guideline, even with there are appropriately sized comps available. Trust me when I tell you, the value of a home can be easily manipulated by the types of comps that are chosen. If an appraiser chooses the cheapest comps available, and the subject property is high-end due to it’s location or features, then the appraisal will come in low. If an appraiser chooses the most expensive comps available, and the subject property is priced fairly, then the appraisal may come in a tiny bit over sales price (about $5000).

By the way, home appraisals will almost never come in more than $5,000 over the sales price. Isn’t that magic? ;-D

Another problem is timing. Using 6-month old homes to value the current market is a little absurd. If you are in a hot “sellers market” then the comps 6 months ago won’t reflect the current market situation. Likewise, if you are selling in a “slowing” market, with lots of homes available, then the price you could have received 6 months ago may not be what you will sell for today (when the buyers have more options).

So all home buyers need to take these things into consideration and they should not treat an appraisal as an absolute TRUTH.

When buying or selling a home, you should keep these things in mind:

In a hot “sellers market” where there are few homes on the market, and most homes have multiple offers within a few weeks of listing, buyers should expect to pay the listing price or more to get a home under contract. The problem with this scenario is that the home may not appraise for value (the sales price).

In a “buyers market,” where there is high inventory (lots of homes available) and buyers have lots of options, then sellers should not expect to receive top-dollar for their property, and it may take longer to find a buyer unless your home is immaculate.

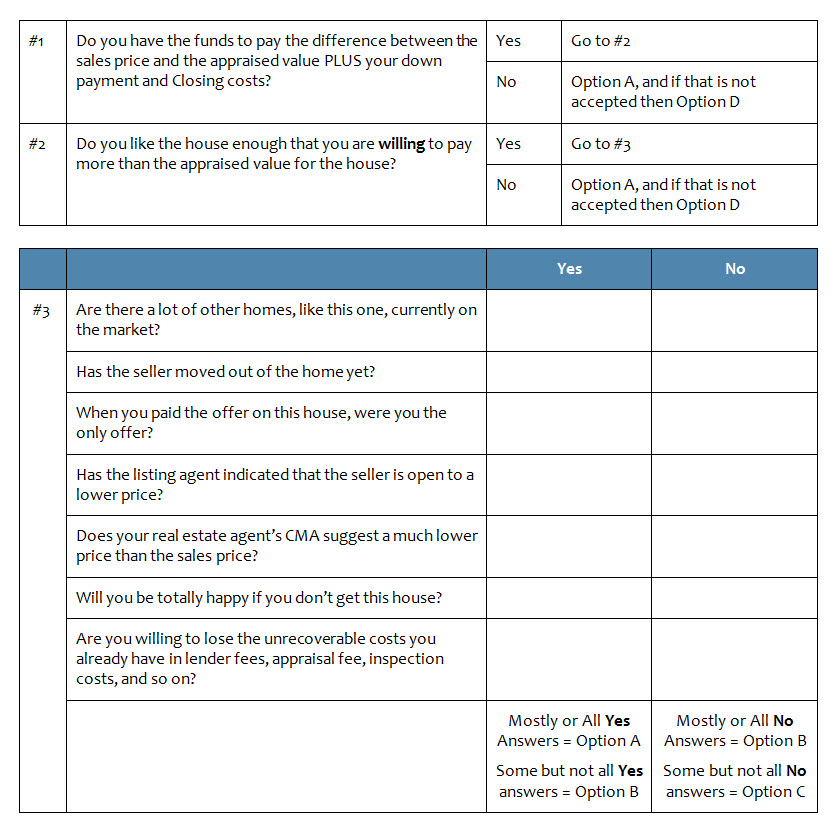

Options for Handling Low Appraisals

If you are a home buyer, and my client, then it’s my job to help you get the home that you want…even if it may at the higher end of the market. If you put a $400,000 contract on a home AND have an appraisal addendum, and then the appraisal comes in at $380,000 (these prices are just examples), then you have four options:

A. Ask Seller to Drop Price to Appraised Value: Send an Amendment asking the seller to agree to change the sales price to match the appraised value. Consequences: If seller agrees, then you get the house at a much lower price. If not, you lose the house and all fees you have already paid, but you get your earnest money back. Sellers do not have to agree to drop the price. If it’s a hot market, then the seller can relist, get another offer, and end up with a different appraisal. (Except FHA appraisals stay for 6 months, but the seller can just refuse FHA offers in the future.)

B. Ask Seller to Drop Price Part Way: Send an Amendment asking the seller to agree to change the sales price to meet you somewhere between appraised value and current sales price (such as at $390,000, or any number between $380,000 and $400,000). Consequences: If seller agrees, then you get the house at a lower price than you agreed to in the contract. But again, the seller does not have to agree to this and can always put the house back on the market.

C. Buyer Pays Extra for House: Move forward with the transaction and pay the extra money between the appraised value and the sales price. This will be in addition to the down payment and other Closing costs. This is not usually recommended, but sometimes necessary to get the home you really want. Consequences: Buyer pays more than originally intended, but gets the home.

D. Terminate Contract: Terminate the contract and get your earnest money back. Consequences: You don’t get the house you want and you lose the fees paid to lender and inspectors.

How Do You Choose the Right Option?

Use the chart below to help find the right option for your situation:

How To Price a Home

NOTE: This video is for normal markets and may not apply to “hot” seller’s markets where most homes have multiple offers.

by Sheila Cox, Five Star Realtor | Updated April 2026

Pricing a Katy home correctly is more complicated than simply comparing the list price to the sales price. Clients often ask me how much they should pay for a home, and I tell them, “It depends on how much it’s worth!” For example, if a house is listed at $450,000 and you get it at $400,000 that may seem like a good deal…but not if the market data says it’s only worth $350,000. (I’m using large numbers here to make the point.) Similarly, if a house is listed at $450,000 and you get it for $450,000, but the market data says it’s actually worth $500,000…then you got a good deal, even though you paid “full price.” See what I mean?

By the way…that new home specialist at the builder’s model home you like will tell you that the $440K model home was originally listed at $520K…sounds like a great deal, right? But they won’t tell you that the last five homes they sold, with that exact floorplan, had an average sales price of $400K. But I will! I’m looking out for you…not the builder.

Home Value Is Not About Price Per Square Foot

Pricing a Katy ome is complicated because real estate market data is changing every month…so home values are changing every month as well. In addition, there is not one price/sf price for an entire neighborhood. Smaller homes in the same neighborhood will typically have a higher price/sf than larger homes in the same neighborhood. Homes with swimming pools and water view lots are generally worth more in the same neighborhood than homes that don’t have those features. Three-car garage homes are worth more than two-car garage homes in the same neighborhood.

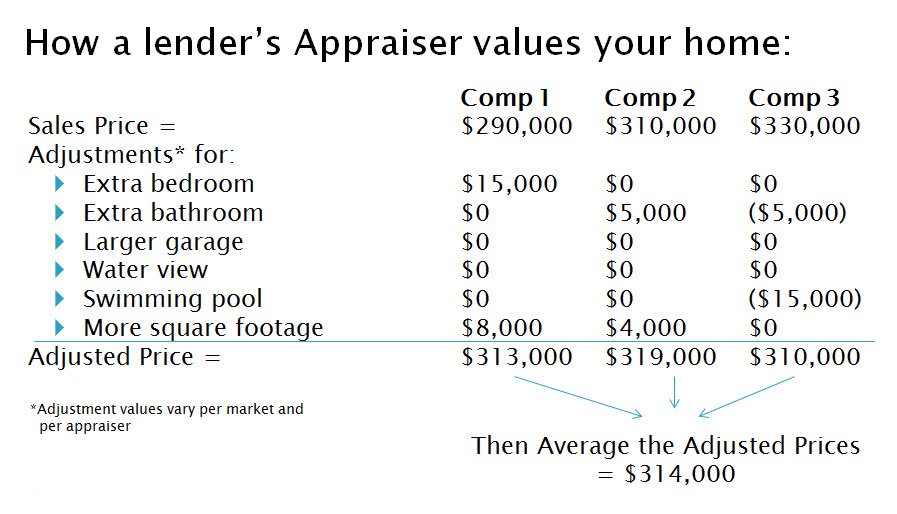

Pricing a home correctly is complicated…you can’t just work off of averages or price/sf. There is no “Kelly Blue Book” value for homes! When determining the value of a home, you should compare at least three to five recently Sold price (not asking prices) for homes that are comparable to the house you want. Comparable means the houses are all within the same size-range (+/- 10%sf), have a similar number of bathrooms, have similar garage sizes, have similar types of amenities and lot types, etc. Usually you will not find three to five homes that are exactly the same as the subject property, so adjustments must be made to the prices, and then the adjusted prices are averaged out. This gives you a good idea of a home’s current market value. See the example below.

By the way, cosmetic items such as granite counter tops, hardwood floors, updated light fixtures, special colors of paint…those items do not typically add value to a home. Appraisers do not make adjustments for most cosmetic items. They try to use Comps that match the home they are appraising. In other words, they don’t compare a “fixer upper” with a totally updated home. As much as possible, they compare “fixer uppers” to “fixer uppers.” So cosmetic adjustments are unnecessary.

New Construction Homes Cost More Than Comparable Resale Homes

New construction homes in a neighborhood make pricing a home correctly more challenging. Technically speaking, investing in a home is very different from investing in an automobile. Homes and real estate are generally “appreciating assets” while cars are generally “depreciating assets.” However, trust me when I tell you that no home buyer on the planet is going to pay the same price for a “used” one-year old home when they can buy a “fresh,” brand-new, never lived in home…where they get to choose all the finishes (paint colors, floors, counter tops, cabinets, etc.). Buyers like that “new home smell” just the same as they like that “new car smell.” And they are willing to pay a premium for the “new home smell” just like they are willing to pay a premium for the “new car smell.”

We all know a car loses value the minute you drive it off the car lot. Likewise, that a new construction home typically loses its value (at least in the short run) the minute that you move in. So do not compare new construction prices with a resale home prices when determining value.

And be prepared to sell your home for less than you paid for it if you bought it from a builder…at least until the builders move out of the neighborhood (and no new construction homes are available) or at least five years (or more) have passed since you bought it from the builder. It is almost impossible to compete on price with home builders when you are selling a resale home. They offer lots of “buyer incentives” to entice buyers to purchase…and they can offer a buyer something you can’t…a never-lived-in-home.

It can be hard to determine what new construction homes are selling for because builders do not always list them on the MLS. Since Texas is a non-disclose state, home builders can sell homes without ever reporting them to the MLS. This often conceals the fact that homes lose value after they are purchased by a builder.

I know that some home sellers think their home is “better than new” because they have done this and that to the home. Home sellers like to price a home based on new construction home prices. But just like a used car, a used home is not usually worth as much to a buyer as a new construction home.

Home Should Appraise for Sales Price

If you are like most home buyers, you are going to get a loan in order to buy a home. That means the lender’s appraiser is going to have a say in how much you can pay for a home. This is something that home buyers and sellers have to be reminded about. It really doesn’t matter if you are willing to pay $450,000 for a house if the lender’s appraiser says it’s only worth $420,000…unless you want to pay the $30,000 difference at Closing.

Remember that a lender is making an investment in you and your home when they loan you money to buy a house. They want to make sure the home is a good investment. They don’t want to invest more than the item is worth. Always keep this in mind when you are applying for a loan.

Always make sure you have a way to get out of the deal if the home doesn’t appraise for the sales price. That will give you leverage to renegotiate the price if the appraisal comes in too low. If you have a back-out addendum in place, and the appraisal comes in too low, then you have four options:

Get the Seller to come down in price to the appraised value

Meet the Seller somewhere in-between the sales price and the appraisal price (but you will have to pay your share of the difference at Closing)

Pay the difference between the sales price and the appraisal value at Closing…on top of your other down payment and Closing costs

Back out of the deal (but then you will not get back all the money you spend on inspections, appraisal, etc.)

Some people think they will be able to terminate a transaction if the appraisal comes in too low because they believe a lender will not approve the loan in that case. This is not, necessarily, true. If you have enough cash on hand to pay the difference, then the lender may still approve the loan.

Tax Appraised Values Do Not Equal Market Value

Pricing a home based on the “tax rolls” and tax appraised values does not work in Texas. Tax appraised values are usually not accurate for market value in this state. The following short video proves that the tax appraised value is usually (not always) lower than the market value.

Plus, Texas is a non-disclose state and only members of the MLS have actual sales data.

And even Zillow only gives themselves 1-star on their Zestimate’s accuracy (see here).

There is a method for doing a proper Comparative Market Analysis for a home that is similar to how a lender’s appraiser is going to determine a home’s value. Hire an experienced agent who knows what they are doing! (See My Sample CMA)

As your Buyer’s Agent, when you find a home you want to make an offer on, I do a complete CMA (Comparative Market Analysis) and provide you with the data that I have, to determine the realistic and accurate price for a home. This method is similar to how lender’s appraisers value a home. That way you don’t find yourself wasting a lot of time on a home that will not appraise for sales price.

Often times a home is listed at a price that is considerably more than the CMA value. For example, a home that just hit the market may be listed at $550,000 and the CMA, which is based on comparable homes SOLD in the past six months) says it is only worth $500,000. But you, the Buyer, really want the house. What do you do? Well…

Neither the Buyer’s Agent or the Listing Agent can make a seller accept your reasonable offer. And if the house just hit the market, then it’s possible that the seller hasn’t “come to their senses” yet. Sometimes it takes time for a home seller to see that their home isn’t worth what they want for it. If the house sits on the market for months, then sellers either decide to lower the price (hopefully) or they take the home off the market, because they find out they can’t get what they want for it at the current time. (So they will wait.)

I have seen it time and again where a Buyer’s Agent shows the Listing Agent their data for the $500,000 offer and it doesn’t matter…until months go by. Then, eventually, the Seller finally sells the home at the price you offered (or lower)…after letting it sit on the market for 6 months. It is often the case that only TIME can motivate a seller to accept a reasonable offer.

So what do you do if you really want a house that is overpriced?

Do you have time to wait? If so, give it a month or two and hope that another buyer doesn’t beat you to it. If you don’t have time to wait, then move on and find another home.

Pay the higher price. Sometimes it is worth paying more for a house to get what you want, when you want it. And besides…paying a higher price helps raise the prices in the neighborhood…thereby increasing the value of your investment.

Take a risk and offer the price the seller will accept while hoping the appraisal will come in low so you can renegotiate. Use the lender’s appraisal as your “checks and balances” for the price. This strategy can only work if you have the right to back out of the transaction if the appraisal comes in low.

Sometimes an appraisal comes in much higher than what a Buyer’s Agent thinks the house will appraise for. This may be because the market has changed in the 4-6 weeks between the time the agent did the CMA and the time the appraisal is done..and more homes sold in that time. Or sometimes it seems that appraisers choose odd “Comparables” to make the appraisal come in higher (or lower). You just never know what a lender’s appraiser will do when valuing a home.

Negotiating Tips for Buyers

Here are some tips to help with negotiations:

Don’t let yourself “fall in love” with a house, making detailed plans for remodeling and decorating, before you have an executed contract. If you are emotionally attached to the home, then it will be harder for you to walk away from an over-priced home.

Don’t expect to get a seller to go down substantially in price when the house has only been on the market for a few weeks. Be willing to pay a reasonable price instead of getting a “killer deal” on a house that just hit the market.

Don’t low-ball a house in a HOT market when you may get in a competitive situation with other buyers. Be willing to pay a reasonable price (or slightly more) because other buyers will be willing to do so.

There is a funny saying in real estate: “You can’t fix stupid.” That’s just an irreverent way of saying that your Buyer’s Agent can’t prevent other buyers from overpaying for a home. Cash buyers commonly pay way too much for a home because they don’t have a lender’s appraisal holding them back. And you don’t know what the other buyer’s circumstances and motivation are…maybe they are too desperate to be conservative about price.

Always consider your “next best alternative” when making pricing decisions. If you are desperate to get a home because you have to move in six weeks, and you have been looking for several months without finding anything else that you like, then be willing to pay more to get what you want. Likewise, if you are not being forced to move in a short-time frame, or you have seen lots of other homes that you like, then you can be “stricter” with the price you pay for a house.

Do not take the CMA value of a home and then subtract from it all the cosmetic changes (paint, flooring, landscaping, pool, etc.) that you want to make to the home. It doesn’t work that way. Cosmetic items do not, generally, effect the value/price of a home.

Remember that both CMAs and Appraisals are opinions of market value. If you have three different appraisers do an appraisal on the same home at the same time, you will probably end up with three, different values.

Always remember that the price you pay effects the prices in the neighborhood where you are buying and investing. Driving too hard a bargain on your future home can have a negative impact on your home’s value too.

How’s the Katy Real Estate Market?

Get the Report!

What’s Included

Ten-year trend of median sales prices by ZIP Code and neighborhood…so you have a baseline in determining a home value.

Ten-year trend of sales volume by ZIP Code and neighborhood…so you can see which are the most popular neighborhoods.

Ten-year trend of median Days on Market by ZIP Code and neighborhood…so you can see how long it takes to sell a home in each area.

List of the most popular neighborhoods in the Katy area…see what neighborhoods are HOT!

List of the neighborhoods by price (high to low) in the Katy area.

Detailed market data on the most popular Katy neighborhoods

As a homeowner in Texas, your Homestead Tax Exemption is a large exemption to reduce the amount of property taxes you pay. Applying for a Homestead Tax Exemption (more info) is a one-time activity in Texas that homeowners need to do the first year they buy a home…not something you do every year. The deadline is not until the first one-year anniversary of Closing on your home, however, you can do it now.

Your application must include a copy of your Texas Driver’s License or DPS Identification Card and the address on the driver’s license or identification card MUST be the same as the address on which you are filing an Application for Residence Homestead Exemption (because you can only get this exemption on ONE home you live in). Make an appointment to get your Texas driver’s license here.

When you purchase a resale home, you can purchase a home warranty (a.k.a., Residential Service Contract or RSV) that will protect you against most ordinary flaws and breakdowns for at least the first year of occupancy. The warranty may be paid for by the Seller for the first year. That cost can be $600-800 (or more) depending on the plan you select.

A home warranty program will give you peace of mind, knowing that the major covered components in your home may be repaired by the warranty company, if necessary. If you need help deciding on a home warranty company, check out Top Ranked Home Warranties.

Even with a warranty, you should have the home carefully inspected before you purchase it.

Will Prior Foundation Repairs Effect a Home’s Resale Value?

In Texas, there is a saying that all houses here either have foundation repairs or will need them in the future. That’s because the soil in most parts of Texas is an “expansive soil” that significantly expands and contracts based on the level of moisture in it. And since Texas is known for either droughts or floods…our soil tends to expand and contract a lot.

That is why it is very important for homeowners to keep the soil around their home evenly watered. Water in the soil provides pressure to support the home. During a drought, the lack of moisture may cause a foundation to sag. Simply watering the soil can often push a slightly sagging foundation back up…no kidding!

Does having a prior foundation repair on a home effect the resale value? That’s a controversial question with no “scientific” data to prove one opinion or another. Some say that as long as the repair is done by a reputable foundation company and has a transferable lifetime warranty…no problem. It may even be considered a positive feature of the home, since the cost of the repair has been covered by a prior owner.

NOTE: If you need some brick or mortar repair in the Sugar Land area, contact JQ Brick at 713-253-5092…they do excellent work at very reasonable prices.

These kinds of cracks do not necessarily mean there are foundation issues…bricks and mortar crack very easily.

They do need to be resealed, however, with mortar (not caulk) to prevent water penetration into the side walls.

Call JQ Brick at 713-253-5092.

Others know that inexperienced home buyers may be scared of purchasing a home with prior foundation repairs…and will not even give such a home a second glance. So, by reducing the number of prospective buyers for a home this way, it could have a negative impact on the price per square foot that home can command. That would suggest that a home buyer should not pay a neighborhood’s top price/square foot for a home with prior foundation repairs…unless there are other special features that significantly override the foundation issues.

Before a home owner puts a brick home on the market to sell in the Katy TX area, a thorough inspection on the exterior of the home should be performed. All the walls should be checked for cracks along mortar lines and brick. The lintels above windows and doors should be checked for rust. Make sure that you look behind hard-to-see areas covered with bushes as well.

These kinds of cracks do not necessarily mean there are foundation issues…bricks and mortar crack very easily. They do need to be resealed, however, with mortar (not caulk) to prevent water penetration into the side walls. Call JQ Brick at 713-253-5092.

If you find any cracked brick or mortar, or rusted lintels, requiring brick repairs, then call a brick restoration company to have them repaired before you put the house on the market. If a potential home buyer sees these kinds of cracks, it may scare him away before he takes a serious look at the home. Or, if the cracks are found during an inspection, it can kill the deal. These brick repairs are relatively inexpensive (usually around $500 or less) and need to be done whether you sell or not…to prevent water penetration into the side walls.

Cracks in bricks and mortar may indicate foundation issues, but they definitely do not mean that the foundation definitely has problems. I’ve seen homes with cracks running the entire length of the home that did not require foundation repairs even after inspections by several foundation repair companies. However, most home buyers are not foundation experts and automatically think there are foundation problems when they see cracks in the walls…and move on to the next house to consider buying.

In Texas, there is a saying that all houses here either have foundation repairs or will need them in the future. That’s because the soil in most parts of Texas is an “expansive soil” that significantly expands and contracts based on the level of moisture in it. And since Texas is known for either droughts or floods…our soil tends to expand and contract a lot…causing the need for brick repairs on a regular basis.

That is why it is very important for homeowners to keep the soil around their home evenly watered. Water in the soil provides pressure to support the home. During a drought, the lack of moisture may cause a foundation to sag. Simply watering the soil can often push a slightly sagging foundation back up…no kidding!

Katy Home Security: Tips for Securing Your Home That Are Not Well Known

If you are interested in Katy home security, then let me tell you my story…

A while back I had the unfortunate experience of having my home burglarized.

I thought my home was pretty safe:

It’s in a low-crime neighborhood with active police patrols.

I have an alarm which I always activate when I leave.

I had good quality, double-key locks on all my doors.

I have two, small, barky dogs.

But in spite of all that, my front, side door (next to the garage, but on the front of the house) was kicked in at 2:25 p.m. on a school day…in the middle of the afternoon! I always thought break-ins happened at night! But here’s what I found out when I researched home security.

Your Door Is Easy to Kick In

When I researched how to prevent break-ins, I came across some interesting facts that I did not know. One of the best articles on home security that I read was “Home Security: Burglary Prevention Advice” by Chris E McGoey, CPP, CSP, CAM at http://www.crimedoctor.com/home.htm

That article points out:

“The most common way used to force entry through a door with a wooden jamb is to simply kick it open. The weakest point is almost always the lock strike plate that holds the latch or lock bolt in place followed by a glass paneled door. The average door strike plate is secured only by the soft-wood doorjamb molding. These lightweight moldings are often tacked on to the door frame and can be torn away with a firm kick. Because of this construction flaw, it makes sense to upgrade to a four-screw, heavy-duty, high security strike plate. They are available in most quality hardware stores and home improvement centers and are definitely worth the extra expense. Install this heavy-duty strike plate using 3-inch wood screws to cut deep into the door frame stud. Use these longer screws in the knob lock strike plate as well and use at least one long screw in each door hinge. This one step alone will deter or prevent most through-the-door forced entries. You and your family will sleep safer in the future.”

So now I tell all my friends, family, clients–EVERYONE!–that they need to secure their strike plates with 3.5 inch screws. It doesn’t matter how good your lock is, if all a thief has to do is kick in the door and bust the doorjamb! These screws are inexpensive and easy to install no matter how “tool challenged” you may be. (Read Consumer Reports article)

You Need Better Locks

The second thing that I did to improve home security, was to replace my double-key locks with The Ultimate Lock which was designed by a former Houston police officer and are made right here in Fort Bend County! These things are incredible. They have a safety pin which, when pushed in, prevents even a person with a key from unlocking the door. You can buy them at Lowes for about $180 each.

NOTE: The only thing that I don’t like about these locks is that they are not double-key locks…so if your door has glass around it, you will need security film to prevent a thief from breaking the glass to unlock the door (see below).

Even if you don’t install the Ultimate locks, you should at least add a “landlord lock” to your exterior doors. These are locks without keys that protect you when you are inside the home…so they are used for preventing home invasions. I buy these off of Amazon and install with 3.5″ screws.

Another thing that I learned about home security is that if they can’t kick your door in, then they will probably “smash and grab” a window…most likely a master bath or master bedroom window, because most people keep their valuables and prescription medication in the master bathroom or closet. I am good friends with two police officers who have security film on their windows to prevent this. Plus, I asked a Fort Bend Sheriff’s deputy to give my house a security audit, and he too has security film on his home windows. That’s 3 out of 3 police officers that I know who have security film on their own homes. So I contacted Steve Meyer, at SunTech Glass Tinting, to install security film on my windows too…especially all the windows next to my doors and locks!

There are many different brands of security film, but you have to check out a video demonstration to believe it.

You can search on YouTube for “security film for windows” and see lots of different demonstration videos. The cool thing about this stuff, is not only does it improve the security of your home, it’s also a layer of protect from flying debris…say, during a hurricane. I think…that’s good…one less thing.

—by Sheila Cox, Five Star Realtor | Updated April 2026—

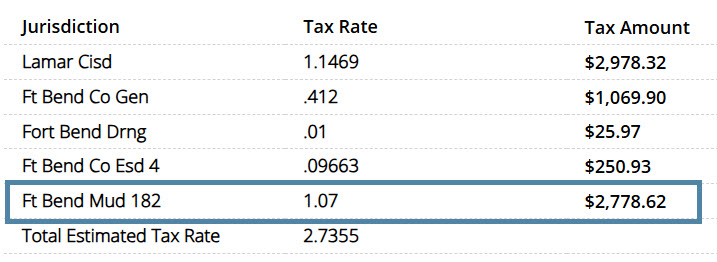

Katy TX Property Taxes–Unfortunately, property taxes in Texas are among the highest in the country. But before you panic, just remember that we don’t have a state income tax in Texas…so one sort of offsets the other. I tell my out-of-state clients to find out the state income taxes they paid last year and add that to their property taxes, and then compare that number to the property taxes here.

Each Katy subdivision (and there are over 200!) has different property tax rates…and they can change from year to year. Subdivisions in our newest neighborhoods, like Firethorne and Tamarron, tend to have the highest property tax rates (3.2 to 3.6) and subdivisions in our older neighborhoods, like Kelliwood or Nottingham Country, tend to have the lowest tax rates (2.2 to 2.8).

Older homes within the same neighborhood

may have lower tax rates than newer homes in newer sections.

The tax rate in a subdivision tends to go down over time. That doesn’t mean your taxes go down over time, because the home value is probably increasing, but your tax rate will probably decline with time.

One thing I like to point out though…our newer homes tend to be much more energy-efficient than our older homes; so you will save money in energy costs when you buy a newer home. That may help partially offset the higher taxes.

There are tax benefits and other benefits in owning your own home (which can make up for the high Katy property taxes). Please read The Benefits of Home Ownership to learn more.

Something else you need to know…the tax appraised value on a home does not usually equally the market value of the home in Texas. If a home is older, it’s tax appraised value may be significantly lower than it’s market value. So don’t use those numbers when calculating a sales price!

In most parts of Fort Bend County, neighborhood infrastructure is provided through a Municipal Utility District, commonly called a MUD. A MUD is a special-purpose local government entity created under Texas law to finance, build, and maintain essential utilities for a specific area—usually a residential community.

When a new subdivision is developed, the developer often forms a MUD to fund infrastructure such as water lines, sewer systems, drainage facilities, and sometimes roads, parks, or recreational amenities. Instead of the developer paying the full cost upfront, the MUD issues bonds to build these improvements. Those bonds are then repaid over time through property taxes collected from homeowners within the district.

For homeowners, this means that your property tax bill will typically include a separate MUD tax rate in addition to county, school district, and other local taxes. The MUD uses those tax revenues to repay infrastructure bonds and operate the district’s utilities. With a MUD you will have a monthly bill that covers your water, sewer, and trash service. In addition to that, your property taxes will include a portion that goes to the MUD. So they do add to your property tax bill.

#image_title

A MUD is governed by a board of directors, usually elected by residents who live within the district. This board makes decisions about budgets, tax rates, and ongoing infrastructure maintenance.

MUDs are very common in fast-growing suburban areas like Fort Bend County because they allow new communities to develop without requiring existing taxpayers in nearby cities to fund the infrastructure. There are PROs and CONs of having MUDs to provide utilities, but regardless of our opinions on them, you will be hard-pressed to find many neighborhoods in this area that are not assigned to a MUD.

As a homeowner in Texas, your Homestead Tax Exemption is a large exemption to reduce the amount of Katy TX property taxes you pay. Applying for a Homestead Tax Exemption (more info) is a one-time activity in Texas that homeowners need to do the first year they buy a home…not something you do every year.

The deadline is not until the first one-year anniversary of Closing on your home.

Your application must include a copy of your new Texas Driver’s License or DPS Identification Card and the address on the driver’s license or identification card MUST be the same as the address on which you are filing an Application for Residence Homestead Exemption (because you can only get this exemption on ONE home you live in). Make an appointment to get your Texas driver’s license here.

Here are some helpful tips for Buyers when negotiating a sales offer on a home:

Find out the number of days the house has been “on the market” (also referred to as DOM: Days on Market) as well as the pricing history of the home. In Texas, only members of the MLS will have access to this data…it is not publicly available.

NOTE You cannot use Trulia or Zillow or public tax information to find this information because Texas is a “non-disclose” state on real estate sales figures. Tax records are not accurate sources of real estate sales figure either…the appraised value of a home for tax purposes is usually not related to the actual value or price of the home.

Ask the Seller’s agent why the home owner is selling the home. That agent does not have to answer the questions (due to client confidentiality) but typically will. This helps you understand the Seller’s motivation behind the sale.

Make sure your Realtor does a Buyer’s CMA (comparative market analysis) to determine the current, probable value of the home. This will prevent you from over-paying for the home and will also prevent you from wasting your time. For example, lender appraisals these days in our area tend to the conservative side. If a Seller is demanding a price that is $50,000 over the current market value of the home, the lender will not loan the money to you to buy it, even if you are willing to pay it. You will either have to come up with the cash to pay the difference, or walk-away from the deal. Better to know earlier rather than later.

Do not belittle the Seller or the property to the Seller who has strong emotional ties to the home. As much as possible, minimize emotional responses on both sides.

Always make offers or changes to offers in terms in writing…Texas requires written contracts in regards to real estate.

If you view a home when a Seller is present, be as friendly and positive as possible. Sellers like to sell to people they like.

Do not start mentally decorating the house or arranging furniture in too much detail until you have a deal in writing…be ready to walk away. This is the biggest financial investment you may ever make…stay as rational as possible.

Don’t get hung up on a few hundred or even thousands of dollars and lose a deal. You don’t want to lose a good deal on a $500,000 home over a $300 survey (for example).

A real estate “Closing” is where you and I meet with some or all of the following individuals: the Seller, the Seller’s agent, a representative from the lending institution and a representative from the title company, in order to transfer the property title to you. The purchase agreement or contract you signed describes the property, states the purchase price and terms, sets forth the method of payment, and usually names the date and place where the closing or actual transfer of the property title and keys will occur.

If financing the property, your lender will require you to sign a document, usually a promissory note, as evidence that you are personally responsible for repaying the loan. You will also sign a mortgage or deed of trust on the property as security to the lender for the loan. The mortgage or deed of trust gives the lender the right to sell the property if you fail to make the payments. Before you exchange these papers, the property may be surveyed, appraised, or inspected, and the ownership of title will be checked in county and court records.

About a week in advance, I will schedule the real estate Closing with you and the title company. We will meet at the title company on the day of closing, sit in a conference room with an escrow officer (who is also a notary), and you will sign the legal documents to purchase the home.

You will need to bring your driver’s license with you to the real estate Closing. At closing, you will be required to pay all fees and closing costs in the form of “guaranteed funds” such as a cashier’s check. Your agent or escrow officer will notify you of the exact amount at the day before Closing.

Buyers: What To Bring to Your Closing Appointment

Here’s the minimum of what to bring to your “Closing”:

Photo ID

“Good funds” for your down payment and other costs: typically

a cashier’s check or wire transfer—never cash

Please know that a home inspection is one of the most important parts of buying a home. But it can be overwhelming trying to find a reputable inspector who you can trust. I provide all my buyer clients with a list of licensed home inspectorsin the area to make this process easier for you. You should call ahead and “interview” some inspection companies to find the one you want to work with when you get a contract on a house.

In choosing a home inspector, consider one that has been certified as a qualified and experienced member by a trade association.

Ask if they:

a) measure the foundation levels

b) check walls and ceiling with thermal camera

c) provide color photos in report

Also get them to hire your termite inspection. Different inspectors charge different fees and those fees are partly determined by the age and size of the home.

A lot of the time, home inspectors will advise you to have a licensed HVAC specialist check the AC and furnace. If you think this will be an issue (because the house has an old HVAC system), you should set that appointment up in advance as well. Here are a couple of suggestions:

Bill Anderson Air at 281-398-1823

Fresh Air Inc at 281-747-5166

Hartford Services at 281-261-3333

NOTE: Make sure the HVAC company understands this is an INSPECTION and you don’t own the home.

One thing to note…it’s challenging to test an AC in the winter time. For ACs you want at least a 15 degree differential, but 17 or 18 degree differential is the best. If the outside temperature is below 72 degrees, then an inspector may not be able to get an accurate reading.

Home inspections should include information and photos on the condition of the following:

Appliances

Plumbing

Electrical

Air conditioning and heating

Ventilation

Roof and Attic

Foundation

General Structure

Keep in mind that NO HOME IS PERFECT, not even new construction, and you should be prepared for $1000-3000 worth of repair issues listed on an inspection report (maybe more, depending on the age of the home).

What Is Inspected

The home inspection is designed to report on any actual or potential defects or problems with the home that may require repair. Not everything they report will be considered an actual defect by you; you must decide on whether or not the items noted require repair or not for your peace of mind. For example, I rarely see a home inspection report where the inspector does not note that the dirt is too high around the foundation of the home. This seems to be something that they always note because it could potentially hide termite activity around the home…and inspectors have to protect themselves against potential lawsuits. But this is something that you can easily fix when you move into the home.

Homes are on a 17 year cycle (approximate) meaning that a lot of high-ticket items will “wear out” when they are about 17 years old. Be aware of that when looking at homes that are about that age or slightly more. High ticket items include roofs, HVAC systems, and water heaters.

NOTES

Should serious foundation or structural problems be indicated, the inspector will recommend that a structural engineer or other professional inspect it as well. This may include hydrostatic testing (which requires special permission from the Seller).

Stucco inspections are very important and require special permission from the Seller because they are “invasive.”

The home cannot “pass or fail” an inspection, and your inspector will not tell you whether he/she thinks the home is worth the money you are offering.

Inspectors must base their findings on current building codes and best practices, but homes built 10, 20, 30 years ago were built with different codes and best practices. An older home does not need to be “brought up to code” and get a new building permit. A buyer needs to decide what they can live with and what they cannot live with.

According to the Texas Real Estate Commission: “A home inspection is a limited visual survey and basic performance evaluation of systems and components of the house. It does not require the use of specialized equipment and is not a comprehensive investigative or exploratory probe to determine the cause or effect of deficiencies noted by the inspector.”

I recommend being present for the last hour of the inspection. (It distracts the inspector if you are there the entire time, and then they miss things.) This is to your advantage because you will be able to ask questions, and get tips for maintenance, and a lot of general information that will help you once you move into your new home. Most important, you will see the home through the eyes of an objective third-party. But always keep in mind that an inspector’s job is to report on all potential issues (like dirt too high around the foundation) and you need to be reasonable in your repair request negotiations with sellers.

Never send an inspection report to your lender and avoid putting a long list of repairs in an Amendment, or it may impact your home loan.

Common Issues on Inspection Reports

The most common issues that appear on inspection reports in this area are listed below. The repair prices in the Usual Consequence column or approximate estimates only to give you some idea of the repair cost. You will need to get real estimates on the specific home.

Issue

Usual Consequence

HVAC not cooling properly

Usually you can have the HVAC serviced for around $500 or less and get it working properly, but if it is a really old (15 years or more) then you may be looking at major replacement costs, part of which may be covered by a Home Warranty.

Old furnace (20 years or more)

Since furnaces are not used in this region very often, they seem to last a long time! You may want to have a HVAC specialist check to make sure the heating element is in good condition…home inspectors cannot do this.

Electrical panel has issues or wrong size breaker on the HVAC system

You should be able to find an electrician to replace the electrical panel (worst case scenario) for $1500 or less. Other minor issues, such as wrong sized breaker, will cost much less.

Soil too high around foundation

You can use a shovel to lower the mulch/soil around the foundation or hire your “yard guy” to do it.

Grading/drainage issues

Minor issues can be fixed with a shovel and dirt. Major drainage issues may require a “french drain” type of solution that could cost $1500-2000. New construction homes often have drainage issues that need to be worked out.

Minor roof issues with flashing or a few raised shingles.

Find a roofing company to make the repairs which are often under $500.

No sediment trap on gas line to water heaters and furnace or other ventilation issues with those two appliances.

A licensed plumber will usually install sediment traps (for safety) for around $200/appliance. Ventilation issues may have other minor repair costs.

No (or non-working) GFCI outlets in kitchen or bath.

This is commonly MIS-reported. Inspectors often say the GFCIs don’t work when they do. A handyman can replace a GFCI outlet on most homes for $100/outlet.

General plumbing issues like leaky faucets or slow drains

A handyman or plumber can usually fix these items for minimum cost.

Deferred maintenance

Exterior windows, doors, and siding need to be caulked on a regular basis (every 2-5 years) to prevent water penetration. Masonite siding must be kept well-sealed and painted with high quality paint or it will rot. Expansion joints must be sealed with special sealant to prevent water penetration.

Sprinkler problems

Sprinklers heads often get broken by lawn mowers and sometimes the backflow preventor needs to be repaired, usually for less than $500.

Cracks in exterior brick due to settling

Cracks in brick need to be sealed with mortar to prevent water penetration. Hire JQ Brick to do this…usually for less than $500.

Settlement cracks in sheetrock

It is very common to see settlement cracks in the interior sheet rock, especially at the corners of an angled ceiling. These can be covered and painted by a you or good painter.

Pool equipment

If the home has a pool, then the pool equipment may have issues. This is a common area where you will get INFLATED repair estimates. Make sure you hire the right company for repair estimates. Pools are a constant maintenance issue, especially the Polaris cleaners.

Foundation issues*

NOTE: “Corner pops” are not foundation issues.

If the foundation level differentials exceed 3 inches in an area, then you will need to get a foundation repair estimate. Foundation repairs can range from $5,000 to $20,000 or more, depending on how many piers need to be installed. Make sure you learn about foundations by reading: “Buyer’s Guide to Slab-On-Ground Foundations.”

To properly maintain your foundation, make sure you use a sprinkler system to keep the soil evenly hydrated. Sprinkler systems are very important for your foundation maintenance!

*Not a very common problem, but may pop up occasionally.

After the Inspection

Once the inspection is completed, you will have three options to take (*assuming you purchased a Termination Option) in the original contract:

Terminate the Contract – If any serious defects are found with the home, then you can exercise your Termination Option*, lose your Option Fee, but get your earnest money back.

Ask for Repairs – If you do not have the cash on hand to make the repairs that you deem important, then you can ask the Seller to make those repairs in an Amendment to the sales contract. However, keep in mind that this is not recommended because home owners tend to hire the cheapest repairs possible and it’s not guaranteed that repairs will be done in a satisfactory manner.

Ask for a Seller’s Contribution to Closing Costs – If you would rather ensure the repairs are done to your satisfaction, then request a Seller’s Contribution to Closing Costs (SC) which is a credit at Closing that will provide you with more cash on hand, after the completion of the sale, so that you can hire your own repairs.

In Texas, the home inspection phase is often referred to as the “Option Period.” Watch my video for an explanation…

Even if you do not purchase a Termination Option, you still have the right to inspect the home. You just do not have the UNRESTRICTED right to back out of the deal and get your earnest money back. Even if you have a Termination Option, that does not guarantee that the Seller will agree to any repair requests or price reductions.

Are you worried about whether home buying is a good INVESTMENT?

Buying a first home can be an intimidating process. But the first step is making those first decisions: I want to own my own home; I can afford to own my own home; owning my own home makes sense for me financially and emotionally. If you are still struggling with those first decisions, here are some facts that might help you make that first step towards becoming a homeowner.

You Can’t Afford NOT to Buy a Home!

Over the last ten years, the cost of rental housing in the U.S. has increased an average of 3 percent per year. That means that an apartment or home renting for $750 per month will cost more than $978 a month in ten years. If you rent the same home for ten years, the total amount you would pay for rent will equal $103,000!

Tax Advantages of Owning a Home Result in Savings

None of that $103,175 is returned to you, either through savings or as an investment. Homeownership, on the other hand, has tax advantages over renting a home, and those advantages can help you save money. Unlike your monthly rent, part of your monthly mortgage payment “comes back to you” in tax savings. Here’s an example:

You purchase a home that costs $110,000 (plus closing costs – expenses incurred to actually process the transaction). You finance the balance with a 30-year fixed rate mortgage at 6.5 percent interest. Your monthly payments (not including utilities, maintenance, insurance, etc.) are:

You actually save $195 a month by owning your own home. On a yearly basis, the savings is even more dramatic:

Homeownership is a Good Investment

For the majority of Americans, their home is their largest financial asset and a major player in their investment portfolio. It’s a good thing, too, since stock market value has declined since 1998, while home price appreciation has increased. The NATIONAL ASSOCIATION OF REALTORS® estimates that home value rises, on average, by 4.5 percent a year. That’s a steady return on investment; one’s own home is a much less volatile asset than stocks, bonds or mutual funds.

As an example, let’s look again at that $110,000 home. Unlike your rental unit, your home should appreciate over time. Assuming a 4.5 percent appreciation rate, your home will be worth $114,950 in the second year of ownership, $120,123 in the third year of your owning it, etc. After ten years, your $110,000 home will be worth $163,470. Not only do you earn a rate of return on your original purchase price, but you also get a return on any subsequent appreciation.

Homeownership Builds Wealth for Households

The Federal Tax Reserve Board estimates that homeowners have a net worth almost 36 times more than that of renters. In 2001, the median net worth for homeowners was $171,700 compared to $4,800 for renters. How do you build up your net worth? Through those “appreciating returns” on your home.

We’ve already seen how your $110,000 home is worth $163,470 in ten years. In addition, you are paying down the principal on your mortgage. Remember that $100,000 you borrowed at 6.5 percent over 30 years – that debt amount is decreasing every month and every year.

After the first year, you now only owe $98,786 on a home that is worth $114,950. You have “netted” a $4,950 increase in the value of your home, plus $1,116 a year that previously you owed as part of your mortgage debt. As your debt decreases and the home value increases, you accumulate wealth from the value of your home. In addition, over this ten-year period, you will have a significantly lower after-tax payment for housing. Each year as your home appreciates and you continue to pay down your mortgage debt, you increase your own net worth.

Homeownership – It’s NOT Just About Money

The “numbers tell the story” should ease your mind about the financial aspects of becoming a homeowner. But there are other, less monetary, benefits to homeownership. Several research studies indicate homeownership adds to the value of communities, has positive effects on children, and even contributes to increased voter participation rates.

—by Sheila Cox, Five Star Realtor | Updated April 2026—

One question that I get a lot is, “What’s recommended: buying new vs resale home in Katy?” A new home is one that has never been lived in while an existing home has been lived in by a previous owner. There are Pros and Cons either way that you should consider. Here are my home buying tips for buying a new vs resale home.

PROs for Purchasing a New Home May Include:

Lower maintenance costs during the first years of owning the home.

Lower energy costs because new homes are built with better energy saving materials and equipment than older homes.

More functional home designs and floorplans as well as up-to-date home fixtures.

Latest technology features such as pre-wired for a home computer network.

Possibly the ability to choose paint colors, floor types and colors, exterior colors, and other optional home features.

NOTE: There is typically a substantial markup on these items.

Builder incentives to lower the initial cost to purchase.

Easier to get to know neighbors because everyone is “new.”

PROs for Purchasing an Existing (Resale) Home May Include:

Lower price per square foot than newly built homes.

Better locations and shorter commute times.

Mature landscaping in both the yard and throughout the neighborhood.

Proven track record of home values in the neighborhood.

Lower tax rates since more neighborhood features have already been paid for by home owners.

Sales contracts that are fair to both parties…not one-sided in favor of the builder.

Lower move-in costs (possibly) since home already has window coverings, landscaping, garage door openers, and other items that you will have to buy for a brand new home.

Easier for home inspector to find home defects because more time has passed since the home was constructed. NOTE: New homes may have hidden defects that are impossible for a home inspector to find.

More established school zone boundaries than for new neighborhoods.

Established community activities and events.

Quicker move-in date compared with building a home from scratch in a new neighborhood.

If you decide to buy a new home, make sure that you check out the builder first: http://houston.bbb.org/consumers/. Also make sure that you hire an inspector.

And don’t forget to bring your Realtor along when you view new home models! Remember: A Realtor’s job is not “just” helping you find a house to buy…there are over 100 tasks that Realtors may perform for you during the home purchase process! Your Realtor should be on your side because she is your agent. The salesperson at the builder’s model home office is not on your side and has no Fiduciary Duty to you. As an employee of the builder, he or she is looking out for the builder’s best interests.

Before you decide to buy a new home, make sure you get up-to-speed on new home builder’s warranties at:

I don’t want to discourage you from buying a new home…Houston has some really great new home builders. But it’s my job to make sure that you have all the information that you need to make a wise buying decision.

Buying a home is a serious legal commitment with important deadlines and possibly large financial losses if you do not meet your contractual deadlines (as established in the contracts that you sign). Always make sure you read the docs you are signing. Discuss deadlines with your real estate agent and put them on your calendar.

Checklist for Home Buyers

Print this checklist and use it to keep track of your transaction.

This list is not comprehensive. There are a lot of steps that your REALTOR® takes care of behind-the-scenes.

Action

Deadline

Contact three or four lenders to determine how much house you can afford. Determine how much money you will need to purchase a new home. Do you have enough? If not, create a budget and start saving now.

Get approved for a loan. Don’t forget to get an preapproval letter! We will need to submit it with an offer to buy a house.

Hire a real estate agent to help you with your purchase. You need a professional looking out for your best interest. Send your Preapproval letter or “Proof of Funds” to your agent (see video).

Do you need to sell your current home? Your agent will help with that too. Get it on the market!

View “Dream Home Alerts” (see video) for homes when they “hit” the market.

Tour homes (see video) until you find the one that meets your specific needs.

Sign the legal paperwork and make an offer to buy the house that you chose. Be prepared to write check for Earnest Money (see video). Be prepared for some back-and-forth negotiations.

Deliver the Earnest Money and Option fee to the title company. TIME IS OF THE ESSENCE! If you don’t deliver the Option fee on time, then you have NO Termination Option.

NOTE: Learn about Option Periods in Texas (see video).

Once the title company “receipts” your Earnest Money and Option Fee, then send the executed and receipted contract to your lender and start the approval process with him/her.

After the sales contract is executed, hire home inspectors to inspect the home as needed (learn more). This will cost $300 to $700 or more, depending on the number and type of inspectors you hire. Depending on the home, you should think about the following inspections:

Discuss insurability with insurance company and get a CLUE report from insurance agent.

Verify the following if they are important issues to you:

· Square footage of home

· Schools zoned to home (but those may change with rezoning in future)

· Property taxes

· Crime in area (contact police department)

· HOA covenants and restrictions (usually online at HOA website)

Negotiate repairs to home as needed. Be realistic…small miscellaneous items should be expected because no home is perfect. Negotiate big-ticket repairs (if any) or walk-away.

Now that you have exact address, compare mortgages and lenders (at least three is recommended). Choose a lender and mortgage and apply for a loan if you haven’t already. Remember, you have a deadline to meet in the sales contract. Be prepared to pay an application fee (approximately $300) and an appraisal fee (approximately $300-400).

Submit items for your loan application (W2s, tax returns, pay stubs, bank statements, etc) as requested by your lender. Time is of the essence! According to the contract, your deadline for Individual Approval and Notice to a Seller (from lender) is à

If you do not get loan approval, then notify your real estate agent immediately.

Check your Title Commitment (learn more) in a timely manner when you receive it. You have only a few days to “object in writing.” Make sure your real estate agent receives a copy.

Review the Lender’s appraisal in a timely manner. You have only a few days to “object in writing.” Make sure your real estate agent receives a copy.

Review the survey in a timely manner. You have only a few days to “object in writing.” Make sure your real estate agent receives a copy.

Re-inspect home, if you choose, based on agreed repairs.

Obtain home owner’s hazard insurance. Make sure you get at least three quotes. Notify your real estate agent which policy you choose. Don’t forget Flood Insurance!

Select your residential service contract (“home warranty”) if applicable and notify your real estate agent (learn more). The title company will order and pay for the home warranty.

Plan your move (get detailed list) and order your utilities to be turned on the day you Close. Always allow a week or more overlap to move out of current home and into new home. Do not plan to Close and move on the same day!

Ask your lender for the amount of money you need to Close. Make sure your funds for Closing are available at local bank. Transferring money from investment accounts can take time…work with your lender and bank and prepare in advance.

Your property MUST reach Lender Approval at least 4 days before Closing otherwise you may not be able to obtain a refund of your earnest money due to default on Closing. If there is a delay in getting the loan, notify your real estate agent immediately.

Make sure your Closing is scheduled. You will need photo IDs, checkbook, and a cashier’s check or wiring instructions from your bank.

You must sign your Closing Disclosures (from lender) at least 3 days before your Closing date or you will not be able to Close on time. If you do not sign the CD in a timely manner, this may put you in default and there could be serious financial consequences.

Get your cashier’s check for funds needed to Close the day before Closing.

Do your final walk-through.

Go to the Closing and bring your funds to Close, a checkbook, and a photo ID for each person (husband and wife). Plan on a 2-3 hour process.

Move into your new home and enjoy!

Make sure you receive a copy of your Deed (from the Title company) within a couple of weeks after Closing. Be prepared for mail “scams” offering to file legal docs for a fee.

Apply for your property tax exemptions as applicable in your state.

Contact three or four lenders to determine how much house you can afford. Determine how much money you will need to purchase a new home. Do you have enough? If not, create a budget and start saving now.

Get approved for a loan. Don’t forget to get an preapproval letter! We will need to submit it with an offer to buy a house.

When you sign up as my client, I will provide this checklist and more in my Ultimate Home Buyer’s Guide.

So you have put a contract to buy a new construction home with a builder and you can’t wait to move in. Buying a home is exciting, especially if you are a first-time home buyer, but buying a brand new home that has never been lived in doesn’t mean the house will be perfect and you won’t have any issues. In fact, the first owner of a home generally has to work out the “kinks” of a new home…kind of like breaking in a new car.

One of the most important things you need to know: Get the home inspected by a licensed house inspector! Again…”new” doesn’t equal “perfect” and you need an expert to find all the things the builder missed (and give the inspection to the builder to fix what needs fixing). In fact, I have seen inspection reports on “brand new” never-lived-in homes that are longer (with more items to fix) than an older resale homes! And if you are building a home “from dirt” then you may want to hire an inspector who will inspect the home in various stages of completion: foundation, framing, wiring and plumbing, and then final (because new construction homes have problems too!).